Table of Contents8 sections

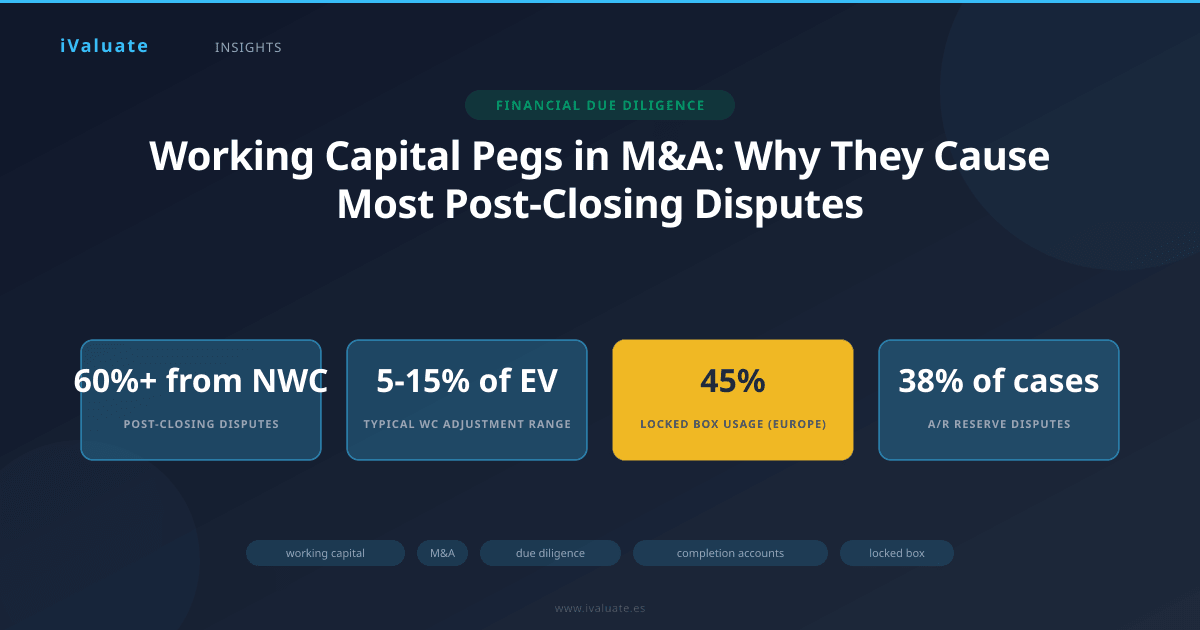

In the complex choreography of mergers and acquisitions, few mechanisms generate as much post-closing friction as the working capital adjustment. Despite being a standard feature in transaction agreements since the 1980s, net working capital (NWC) pegs remain the leading source of purchase price disputes, accounting for over 60% of all post-closing disagreements according to recent studies by major accounting firms. In 2025, as deal activity rebounds following the interest rate normalization period, understanding the nuances of working capital normalization has become more critical than ever for both buyers and sellers.

The stakes are substantial. A typical middle-market transaction might see working capital adjustments ranging from 5% to 15% of enterprise value, translating to millions of dollars in either direction. For a $100 million deal, a 10% working capital shortfall represents a $10 million post-closing payment from seller to buyer—enough to fundamentally alter deal economics and strain relationships between parties who must often continue working together during transition periods.

01 The Economics Behind Working Capital Adjustments

At its core, the working capital mechanism exists to ensure that buyers receive a business with adequate operating liquidity—the financial fuel necessary to maintain day-to-day operations. Unlike fixed assets or intellectual property, working capital fluctuates constantly based on business cycles, seasonality, and operational decisions. A company might show $5 million in working capital on December 31st but only $3 million on March 31st due to seasonal inventory buildups or customer payment timing.

The fundamental principle is straightforward: the buyer should receive the business with a "normal" level of working capital, neither artificially inflated nor depleted. If the seller has extracted excess cash or allowed receivables to balloon and payables to shrink immediately before closing, the buyer deserves compensation. Conversely, if working capital exceeds normal levels at closing, the seller merits additional payment.

In practice, this seemingly simple concept becomes extraordinarily complex. Working capital comprises multiple components—accounts receivable, inventory, prepaid expenses, accounts payable, accrued liabilities, and deferred revenue—each with its own accounting nuances and potential for interpretation disputes. The 2024-2025 period has seen particular complexity around inventory valuation as supply chain normalization has left many companies with excess stock purchased at inflated prices, creating significant valuation challenges.

02 The NWC Peg: Setting the Baseline

The net working capital peg represents the agreed-upon "normal" level of working capital that should exist at closing. This single number, typically ranging from negative figures to tens of millions depending on company size and industry, becomes the reference point for all post-closing adjustments. Setting this peg is where the first major disputes often emerge.

Historical Average Method

The most common approach calculates the peg as the average of month-end working capital balances over a trailing period, typically 12 to 24 months. For example, a business might show the following monthly NWC balances over the past year: $4.2M, $3.8M, $5.1M, $4.5M, $4.0M, $4.8M, $5.2M, $4.6M, $3.9M, $4.3M, $4.7M, and $4.4M, yielding an average of $4.46 million. This becomes the peg.

However, this method immediately raises questions: Should outlier months be excluded? How should seasonal businesses be treated? What if the company was growing rapidly during the measurement period, requiring higher working capital levels? In 2025, many technology companies face this exact challenge, as their working capital needs have evolved significantly as growth rates have moderated from pandemic-era levels.

Last Twelve Months vs. Normalized Approaches

Some transactions use the most recent 12-month average (LTM), while others employ a "normalized" approach that adjusts for known anomalies. A manufacturing company that experienced a one-time raw material shortage might have abnormally low inventory in certain months. Should those months be adjusted or excluded? Private equity buyers, who represented approximately 35% of middle-market M&A volume in 2024-2025, typically push for normalization adjustments that reflect sustainable operating levels rather than historical artifacts.

The tension is inherent: sellers prefer pegs based on recent actual performance (which might be temporarily depressed), while buyers favor normalized levels that ensure adequate operating capacity. A 2025 survey of 200 middle-market transactions found that 73% used some form of historical average, 18% used normalized adjustments, and 9% employed hybrid approaches.

03 The Completion Accounts Mechanism

Under the completion accounts mechanism—the dominant structure in North American M&A and increasingly common in European transactions—the purchase price is adjusted post-closing based on actual working capital at the closing date. This creates a multi-stage process fraught with potential disputes.

The Timeline and Process

The typical completion accounts timeline unfolds as follows:

- Day 0 (Closing): Transaction closes with an estimated working capital level, often based on the most recent month-end balance sheet

- Days 1-60: Seller prepares closing balance sheet and calculates actual working capital

- Days 61-90: Buyer reviews seller's calculations, often with accounting firm support

- Days 91-120: Parties negotiate any differences; if unresolved, disputes move to expert determination

- Days 121-180: Independent accounting expert resolves remaining disputes

- Final settlement: Purchase price adjusted up or down based on final determination

This process creates significant uncertainty for both parties. Sellers may face unexpected clawbacks months after closing, while buyers must potentially fund additional payments or manage disputes while integrating the acquired business. The escrow mechanisms designed to secure these potential adjustments—typically 10-20% of purchase price held for 6-12 months—create their own complications around interest, investment of escrowed funds, and release conditions.

Common Dispute Areas

Analysis of 150 middle-market transactions closed between 2023 and 2025 reveals consistent patterns in completion accounts disputes:

Accounts Receivable Reserves (38% of disputes): The largest source of disagreement involves the adequacy of bad debt reserves. Sellers typically argue that historical collection rates support lower reserves, while buyers point to aging schedules and specific customer risks. A recent case involved a B2B software company where the seller had maintained a 2% reserve based on five-year history, but the buyer identified that 15% of receivables were over 90 days old, with three major customers showing financial distress. The final settlement required an additional $1.8 million reserve, representing a 4% adjustment to the $45 million purchase price.

Inventory Valuation (27% of disputes): Inventory disputes center on obsolescence reserves, lower-of-cost-or-market adjustments, and allocation of overhead costs. The 2024-2025 period has seen particular intensity around these issues as many companies hold excess inventory purchased during supply chain disruptions at prices now above current market rates. Distribution businesses have been especially affected, with some disputes involving 20-30% inventory writedowns.

Accrued Liabilities (19% of disputes): Determining adequate accruals for vacation, bonuses, warranty obligations, and other liabilities requires judgment. Buyers often argue sellers have understated these obligations to inflate working capital. A manufacturing company acquisition in early 2025 saw a $2.3 million dispute over warranty accruals, where the seller had used a 1.5% reserve rate based on recent experience, but the buyer's analysis of product defect trends and new regulatory requirements supported a 3.2% rate.

Deferred Revenue (11% of disputes): For subscription and service businesses, the treatment of deferred revenue creates complexity. Is it a working capital item or an enterprise value consideration? The answer affects both the peg calculation and the closing adjustment. Software-as-a-Service companies, which represented nearly 25% of technology M&A volume in 2024, face particular scrutiny here.

Definition and Scope Issues (5% of disputes): Sometimes parties discover post-closing that they had different understandings of which items constitute working capital. Should customer deposits be included? What about intercompany balances that will be settled post-closing?

04 The Locked Box Alternative

Frustrated by completion accounts complexity and disputes, many European transactions and an increasing number of North American deals have adopted the locked box mechanism. Under this structure, the purchase price is fixed based on working capital and enterprise value as of a historical "locked box date"—typically the last audited or reviewed balance sheet date, often 2-6 months before signing.

How Locked Box Works

In a locked box transaction, the seller guarantees that no value has leaked from the company between the locked box date and closing. The buyer pays a fixed price (often with an interest-like adjustment for the time between locked box date and closing) and assumes all economic benefits and risks from the locked box date forward, even though legal ownership doesn't transfer until closing.

For example, a transaction might sign in March 2025 with a December 31, 2024 locked box date and close in May 2025. The purchase price is based on December 31, 2024 financials, with a 5% annual interest adjustment for the time between December 31 and closing (approximately $2.1 million on a $100 million deal for five months). The seller must demonstrate that no "leakage" occurred—no dividends, management fees, or other value transfers—between December 31 and closing.

Advantages and Trade-offs

Locked box structures offer significant advantages:

- Price certainty: Both parties know the exact purchase price at signing, eliminating post-closing adjustment uncertainty

- Faster closing: No need for post-closing accounting work and dispute resolution

- Lower transaction costs: Reduced accounting and legal fees associated with completion accounts preparation and review

- Cleaner break: Sellers can move on immediately after closing without months of potential disputes

However, locked box mechanisms create their own challenges. Buyers assume all working capital risk from the locked box date, including seasonal fluctuations and operational changes. If a business typically builds inventory in Q1 for Q2 sales, and the locked box date is December 31, the buyer effectively funds that inventory buildup even though the seller retains economic benefit until closing. This timing mismatch can be worth millions in working capital-intensive businesses.

The locked box structure also requires robust leakage protections. Purchase agreements typically include extensive schedules of permitted leakage (normal salary payments, ordinary course expenses) and prohibited leakage (dividends, related-party payments, unusual bonuses). Monitoring and proving leakage violations can be as contentious as completion accounts disputes, though they're generally less frequent.

Market data from 2024-2025 shows locked box usage in approximately 45% of European middle-market transactions but only 15% of North American deals, though adoption is growing. Private equity sellers particularly favor locked box structures when selling portfolio companies, as it provides certainty and allows clean exit. Strategic buyers remain more cautious, preferring the protection of completion accounts when acquiring unfamiliar businesses.

05 Hybrid Mechanisms and Emerging Practices

Recognizing the limitations of both pure completion accounts and locked box structures, sophisticated parties increasingly employ hybrid mechanisms that blend elements of both approaches.

Capped Completion Accounts

Some transactions use completion accounts but cap the potential adjustment at a specified amount or percentage (e.g., ±5% of purchase price). This provides some protection against extreme working capital fluctuations while maintaining price certainty within a defined range. A $75 million transaction might include a ±$3.75 million cap, with any excess adjustment absorbed by the party that would otherwise pay it.

Locked Box with Specific Adjustments

Other deals employ a locked box structure but carve out specific items for post-closing adjustment. For instance, a transaction might use locked box for most working capital components but adjust for accounts receivable collections or inventory levels at closing. This addresses the most volatile or risky elements while maintaining overall price certainty.

Earn-outs and Working Capital

When transactions include earn-out provisions—common in 40% of middle-market deals in 2024-2025—the interaction with working capital mechanisms becomes complex. Should working capital adjustments affect earn-out calculations? If the seller must fund a working capital shortfall, should that reduce the base from which earn-outs are calculated? These questions require careful drafting and often create unexpected disputes during earn-out periods.

06 Best Practices for Minimizing Disputes

After analyzing hundreds of working capital disputes and their resolutions, several best practices emerge for both buyers and sellers:

During Diligence and Negotiation

Define everything explicitly: The purchase agreement should include detailed definitions of each working capital component, including specific account numbers from the chart of accounts. Ambiguity always benefits the party with negotiating leverage post-closing, which may not be the party that had leverage during deal negotiation.

Run sample calculations: Before finalizing the purchase agreement, both parties should prepare sample working capital calculations using recent balance sheets. This often reveals definitional ambiguities or computational disagreements that can be resolved during negotiation rather than post-closing dispute.

Address known issues: If diligence reveals specific working capital concerns—aging receivables, slow-moving inventory, uncertain accruals—address them explicitly in the purchase agreement rather than leaving them for post-closing dispute. A $500,000 reserve negotiated during deal discussions is far less expensive than a $500,000 dispute requiring expert determination.

Consider business characteristics: Seasonal businesses, high-growth companies, and businesses with long cash conversion cycles require special attention to peg-setting methodology. A retail business with December 31 year-end might have artificially high working capital due to holiday season inventory and receivables; using that single date as a peg would be inappropriate.

Post-Closing Execution

Maintain detailed documentation: The party preparing the closing balance sheet (typically the seller under completion accounts) should maintain comprehensive documentation supporting all calculations, reserves, and judgments. Poor documentation invites disputes and weakens positions during expert determination.

Communicate proactively: Rather than presenting a completed closing balance sheet after 60 days, leading practitioners recommend ongoing dialogue between parties during the preparation period. Early discussion of potential issues often enables resolution before positions harden.

Choose experts wisely: If disputes proceed to expert determination, the choice of expert and the scope of their mandate critically affect outcomes. Experts should have deep industry knowledge and clear instructions about whether they're resolving specific disputed items or preparing an entirely fresh closing balance sheet.

07 The Role of Technology and Data Analytics

The 2024-2025 period has seen increasing use of technology platforms to manage working capital analysis and disputes. Advanced analytics can identify historical patterns, flag anomalies, and model different peg scenarios far more efficiently than traditional spreadsheet approaches.

Machine learning algorithms can analyze years of monthly balance sheets to identify seasonal patterns, trend changes, and outliers that should inform peg-setting. Natural language processing can review contracts to identify potential deferred revenue or accrued liability obligations that might be missed in manual review. These tools don't replace professional judgment, but they significantly enhance the quality and efficiency of working capital analysis.

Blockchain-based transaction platforms are emerging that create immutable records of working capital calculations and supporting documentation, reducing disputes over what was agreed or what data was available at various points in the process. While still early-stage, these technologies show promise for reducing the friction and cost associated with working capital mechanisms.

Key Takeaway: Working capital adjustments will remain a source of M&A disputes, but their frequency and severity can be dramatically reduced through explicit definitions, sample calculations during negotiation, appropriate mechanism selection (completion accounts vs. locked box), and proactive post-closing communication. The choice between mechanisms should reflect deal-specific factors including business characteristics, relative negotiating positions, and risk tolerances rather than defaulting to market convention.

08 Looking Forward: The Evolution of Working Capital Mechanisms

As M&A markets continue to evolve in 2025 and beyond, several trends are reshaping working capital practices. The increasing prevalence of subscription and service-based business models is forcing reconsideration of traditional working capital definitions, particularly around deferred revenue treatment. The rise of cross-border transactions is driving convergence between North American completion accounts practices and European locked box preferences, with hybrid mechanisms likely to become more common.

Regulatory changes, particularly around revenue recognition (ASC 606/IFRS 15) and lease accounting (ASC 842/IFRS 16), continue to create complexity in working capital calculations. Transactions closing in 2025 must navigate these accounting standards' implications for deferred revenue, prepaid expenses, and lease-related assets and liabilities. The parties that anticipate and address these technical issues during negotiation will avoid costly post-closing surprises.

Environmental, social, and governance (ESG) considerations are also beginning to affect working capital mechanisms. As companies face increasing obligations around sustainability reporting, carbon credits, and social impact metrics, questions arise about how to treat related assets and liabilities in working capital calculations. A company with significant carbon credit obligations or environmental remediation liabilities must address whether these items constitute working capital or separate enterprise value adjustments.

The sophistication of working capital analysis continues to increase, driven by both deal complexity and available technology. Professional platforms like iValuate now enable dealmakers to model multiple peg scenarios, analyze historical working capital trends, and stress-test different mechanism structures with unprecedented speed and accuracy. These tools don't eliminate the need for professional judgment and negotiation, but they ensure that judgment is informed by comprehensive data analysis rather than limited spreadsheet calculations.

For CFOs navigating M&A transactions, whether as buyers or sellers, mastering working capital mechanisms is no longer optional—it's essential to protecting value and avoiding disputes that can consume millions in adjustment payments and professional fees. The parties that invest time upfront in understanding their working capital dynamics, choosing appropriate mechanisms, and drafting precise definitions will reap substantial benefits in smoother closings and fewer post-closing headaches. In an environment where deal certainty and execution speed provide competitive advantages, getting working capital right has become a critical success factor in M&A transactions.