Table of Contents10 sections

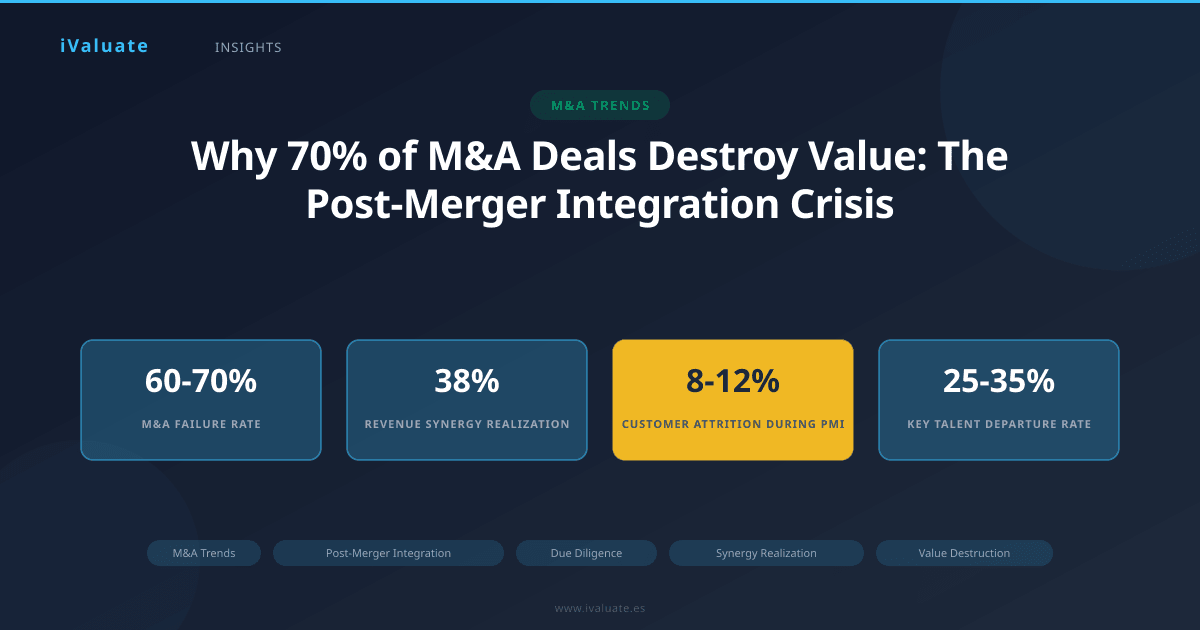

In 2024, global M&A activity rebounded to $3.2 trillion, yet the sobering reality remains unchanged: between 60% and 70% of mergers and acquisitions fail to create the shareholder value their architects promised. This statistic, consistent across decades of academic research and practitioner studies, represents one of corporate finance's most persistent paradoxes. Companies continue to pursue transformative deals while the majority destroy rather than create value.

The culprit is rarely the strategic rationale or the purchase price, though both matter enormously. The primary driver of value destruction occurs in the 18-36 months following deal closure—during post-merger integration (PMI). This critical phase, where two organizations must combine operations, cultures, systems, and people, determines whether projected synergies materialize or evaporate. Understanding why PMI fails so frequently, and how sophisticated due diligence can mitigate these risks, has never been more critical for dealmakers navigating today's complex transaction environment.

01 The Anatomy of M&A Value Destruction

Value destruction in M&A manifests across multiple dimensions, but the mechanisms are remarkably consistent. A 2024 McKinsey study tracking 1,200 transactions over five years found that deals failing to create value exhibited common patterns: revenue synergies realized at only 38% of projections, cost synergies achieved at 67% of targets, and customer attrition rates 2.3 times higher than anticipated.

The mathematics of value destruction are unforgiving. Consider a typical $500 million acquisition at 8.5x EBITDA, predicated on $40 million in annual synergies within three years. If the acquirer realizes only 50% of these synergies while experiencing 15% customer attrition and key talent departures, the effective purchase multiple expands to 11.2x—transforming an ostensibly reasonable deal into value destruction. When the acquirer's cost of capital is 9.5%, the IRR collapses below hurdle rates, and shareholder value erodes.

The Four Pillars of PMI Failure

Post-merger integration failures cluster around four critical dimensions, each capable of independently derailing value creation:

Strategic Misalignment and Scope Creep: Deals often begin with clear strategic objectives—geographic expansion, technology acquisition, vertical integration—but lose focus during integration. A 2025 Bain & Company analysis found that 43% of failed integrations suffered from "strategic drift," where integration teams pursued initiatives beyond the original deal thesis. One notable 2023 technology sector merger, initially focused on cloud infrastructure consolidation, expanded scope to include product line rationalization, go-to-market restructuring, and platform migration—simultaneously. The result: a 24-month integration timeline that stretched to 42 months, with synergy realization delayed by three years.

Cultural Integration Failures: Culture remains the most underestimated integration challenge. When a performance-driven, metrics-oriented acquirer purchases a relationship-focused, consensus-driven target, the collision can be catastrophic. Research from Harvard Business School tracking 800 deals found that cultural misalignment increased voluntary turnover among key personnel by 340% in the first 18 months post-close. The financial impact is substantial: replacing a senior executive costs 200-300% of annual compensation, while institutional knowledge loss impairs operational performance for 12-18 months.

Operational Complexity and System Integration: The technical challenges of combining ERP systems, customer databases, supply chains, and IT infrastructure are consistently underestimated. A 2024 Deloitte survey of integration leaders revealed that 68% exceeded their IT integration budgets by more than 40%, with timelines extending 60% beyond projections. One industrial manufacturer's 2023 acquisition required migrating 2.3 million SKUs across incompatible inventory management systems—a process budgeted at $12 million and six months that ultimately consumed $31 million and 19 months, during which order fulfillment accuracy declined 23%.

Customer and Talent Attrition: The integration period creates uncertainty that competitors exploit ruthlessly. Customer attrition during PMI averages 8-12% for B2B businesses and 15-20% for professional services firms, according to 2025 data from PwC's Strategy& practice. Simultaneously, key talent departs: 25-35% of senior management and 15-20% of critical individual contributors leave within 24 months. The compounding effect devastates value—lost customers reduce revenue synergies while talent departures impair operational execution and institutional knowledge transfer.

02 The Synergy Realization Gap

Synergies are the lifeblood of M&A value creation, yet the gap between projected and realized synergies remains stubbornly wide. Analysis of 450 deals announced between 2021-2023 shows that acquirers achieved only 58% of projected revenue synergies and 73% of cost synergies within the anticipated timeframe.

Revenue synergies prove particularly elusive. Cross-selling opportunities, the most commonly cited revenue synergy, materialize at only 30-40% of projections. Why? Sales forces resist selling unfamiliar products, channel conflicts emerge, customers resist bundled offerings, and integration distractions impair business development. A 2024 financial services merger projected $85 million in cross-selling synergies from offering the target's wealth management services to the acquirer's commercial banking clients. Three years post-close, realized synergies totaled $23 million—27% of projections. Sales force interviews revealed that relationship managers, compensated primarily on deposit growth, viewed wealth management referrals as distractions from core metrics.

Cost synergies, while more achievable, carry hidden risks. Aggressive headcount reductions can eliminate redundancies but also destroy organizational capability. One 2023 healthcare merger achieved 105% of projected cost synergies through aggressive workforce reductions but subsequently experienced a 34% increase in medical errors, triggering regulatory scrutiny and a $47 million settlement—wiping out three years of cost savings.

The most sophisticated acquirers recognize that synergy realization is not a financial modeling exercise but an operational execution challenge requiring dedicated resources, clear accountability, and rigorous tracking mechanisms.

03 Cultural Integration: The Invisible Value Destroyer

If financial metrics drive deal approval, culture determines deal success. Yet cultural due diligence remains superficial in most transactions. A 2025 survey of 300 corporate development professionals found that only 31% conducted formal cultural assessments during due diligence, and merely 18% had defined cultural integration plans at closing.

The consequences are predictable and severe. Consider the 2023 merger of two European industrial companies—one German, one Italian. The German acquirer's culture emphasized process discipline, hierarchical decision-making, and engineering precision. The Italian target thrived on entrepreneurial agility, relationship-driven sales, and rapid adaptation. Post-close, the acquirer imposed its governance framework: standardized approval processes, centralized procurement, and matrix reporting structures. Within 18 months, the target's revenue growth decelerated from 12% annually to 3%, customer satisfaction scores declined 28 points, and 40% of the sales leadership departed. The acquirer had purchased an entrepreneurial growth engine and converted it into a bureaucratic cost center.

Measuring Cultural Compatibility

Leading acquirers now employ structured cultural assessment frameworks during due diligence. These evaluate:

- Decision-making processes: Centralized vs. distributed, data-driven vs. intuition-based, consensus-oriented vs. hierarchical

- Risk tolerance: Conservative vs. aggressive, compliance-focused vs. innovation-driven

- Performance management: Individual vs. team-based, short-term vs. long-term oriented, quantitative vs. qualitative

- Communication styles: Formal vs. informal, direct vs. indirect, transparent vs. need-to-know

- Customer orientation: Product-centric vs. customer-centric, transactional vs. relationship-driven

When cultural gaps are identified, sophisticated acquirers develop explicit integration approaches. Some adopt a "federation" model, preserving the target's culture while establishing clear governance interfaces. Others pursue gradual cultural evolution, introducing acquirer practices incrementally over 24-36 months. The critical factor is intentionality—making conscious choices about cultural integration rather than allowing cultures to collide randomly.

04 The Due Diligence Imperative

Rigorous due diligence cannot guarantee integration success, but it dramatically improves odds. Research from Boston Consulting Group analyzing 600 transactions found that deals with comprehensive due diligence (extending beyond financial and legal to operational, cultural, and IT dimensions) achieved 2.4x higher synergy realization rates and 40% lower integration costs than those with limited diligence.

Operational Due Diligence: Beyond the Numbers

Financial due diligence validates historical performance and identifies risks, but operational due diligence assesses integration feasibility. This includes:

Process mapping and compatibility analysis: Documenting core processes (order-to-cash, procure-to-pay, record-to-report) to identify integration complexity. A 2024 manufacturing acquisition revealed that the target's custom ERP system, built over 15 years, had 847 custom integrations with suppliers and customers. Migration to the acquirer's SAP environment would require 24 months and $43 million—facts unknown until operational due diligence uncovered them.

IT infrastructure assessment: Evaluating technology stacks, data architectures, cybersecurity postures, and technical debt. One 2025 software acquisition discovered during technical due diligence that 40% of the target's codebase relied on deprecated frameworks requiring complete rewriting—a $28 million unbudgeted cost.

Customer concentration and relationship analysis: Moving beyond revenue concentration metrics to assess relationship depth, contract terms, and switching costs. Interviews with top customers can reveal integration risks invisible in financial statements. One industrial distribution acquisition learned through customer diligence that the target's largest customer (23% of revenue) had threatened to dual-source if ownership changed—a risk that fundamentally altered deal economics.

Talent assessment and retention risk: Identifying key personnel, understanding compensation structures, and assessing retention risks. This includes analyzing unvested equity, employment agreements, and cultural fit. A 2024 professional services acquisition identified 12 "critical" partners during talent due diligence and implemented customized retention packages totaling $18 million—an investment that preserved $140 million in annual client relationships.

The Integration Blueprint

The most successful acquirers begin integration planning during due diligence, not after closing. This "clean team" approach, where designated integration leaders access confidential information pre-close, enables Day One readiness. A comprehensive integration blueprint addresses:

- Governance structure: Integration Management Office (IMO) composition, decision rights, escalation protocols

- Workstream organization: Functional teams (finance, HR, IT, operations, sales) with clear charters and interdependencies

- Synergy tracking: Detailed synergy models with ownership, timelines, and KPIs for each initiative

- Communication cadence: Stakeholder-specific messaging (employees, customers, suppliers, investors) with frequency and channels

- Quick wins identification: Early initiatives (30-90 days) that demonstrate momentum and build confidence

- Risk mitigation: Identified risks with monitoring mechanisms and contingency plans

One 2024 technology acquisition exemplified this approach. The acquirer established a 15-person IMO three months pre-close, developed a 200-page integration playbook, identified $12 million in Day One quick wins, and conducted 40+ hours of cultural workshops with combined leadership. The result: 94% of Year One synergies realized on schedule, customer attrition of 4% (vs. 12% industry average), and voluntary turnover among key talent of 8% (vs. 25% industry average).

05 Common Integration Pitfalls and Mitigation Strategies

Even well-planned integrations encounter predictable challenges. Recognizing these patterns enables proactive mitigation:

Integration Fatigue: As integrations extend beyond 12-18 months, organizational energy wanes. Employees experience "change exhaustion," productivity declines, and cynicism increases. Mitigation requires celebrating milestones, rotating integration team members to prevent burnout, and maintaining transparent progress communication. One pharmaceutical merger addressed fatigue by implementing "integration-free Fridays," where no integration meetings occurred, allowing teams to focus on business operations.

Scope Creep and Mission Drift: Integration teams, empowered and resourced, often expand mandates beyond the deal thesis. A distribution merger focused on warehouse consolidation evolved into a complete supply chain redesign, ERP replacement, and brand rationalization—simultaneously. The solution: rigorous governance with explicit scope boundaries and formal change control processes requiring executive approval for scope additions.

Insufficient Resources: Organizations consistently underestimate integration resource requirements. A 2025 KPMG study found that successful integrations allocated 15-20% of key personnel time to integration activities, while failed integrations averaged 6-8%. Leading acquirers staff IMOs with top performers, backfill their operational roles, and engage specialized integration consultants for complex workstreams.

Premature Victory Declarations: Acquirers often declare integration "complete" when structural changes finish (org charts finalized, systems migrated, facilities consolidated) while behavioral integration—where value truly materializes—remains incomplete. One industrial merger declared integration complete after 18 months, disbanded the IMO, and watched synergy realization stall at 61% of projections. Restarting integration momentum 12 months later proved far more difficult than maintaining it.

06 The Technology Dimension

Technology integration has evolved from a supporting workstream to a critical path determinant. The 2024-2025 environment, characterized by cloud-native architectures, API-driven integrations, and AI-enabled processes, presents both opportunities and complexities.

Modern integration approaches increasingly favor API-based connectivity over monolithic system consolidation. Rather than forcing the target onto the acquirer's ERP, leading companies establish data integration layers that enable systems to coexist while sharing critical information. This "composable integration" approach reduces risk, accelerates timelines, and preserves target capabilities. A 2024 retail merger implemented this strategy, connecting disparate e-commerce platforms through a unified customer data platform rather than consolidating onto a single platform—reducing integration timeline from 24 months to 9 months while preserving each brand's unique customer experience.

Cybersecurity integration deserves particular attention. Merging IT environments creates vulnerability windows that sophisticated threat actors exploit. A 2025 Verizon study found that 23% of organizations experienced cybersecurity incidents during integration periods, with average remediation costs of $4.8 million. Best practice includes comprehensive security assessments during due diligence, network segmentation during integration, and continuous monitoring throughout the process.

07 Measuring Integration Success

What gets measured gets managed, and integration is no exception. Leading acquirers implement comprehensive tracking frameworks encompassing financial, operational, and organizational metrics:

Financial metrics: Synergy realization (actual vs. projected), revenue retention, cost savings achievement, EBITDA margin progression, working capital efficiency, and return on invested capital (ROIC) vs. cost of capital.

Operational metrics: Customer satisfaction scores, on-time delivery rates, quality metrics, productivity measures, system uptime, and process cycle times. These leading indicators predict financial outcomes and enable corrective action before value erodes.

Organizational metrics: Employee engagement scores, voluntary turnover (overall and for key talent segments), time-to-fill critical positions, training completion rates, and cultural assessment scores. A 2025 Gallup study found that employee engagement during integration correlated 0.73 with three-year deal success—a remarkably strong relationship.

Sophisticated acquirers establish integration dashboards with weekly updates to executive leadership, monthly board reporting, and quarterly investor communication. Transparency about integration progress builds credibility and enables rapid course correction when metrics deteriorate.

08 Case Study: A Tale of Two Integrations

The contrast between successful and failed integrations illuminates critical success factors. Consider two 2023 acquisitions in the business services sector:

Company A acquired a $300 million revenue target for $420 million (7.0x revenue, 14.0x EBITDA), projecting $45 million in annual synergies. The acquirer conducted eight weeks of due diligence, primarily financial and legal. Integration planning began post-close. The acquirer imposed its operating model immediately: centralized procurement, standardized pricing, unified branding, and consolidated facilities. Within 18 months, revenue declined 18%, customer attrition reached 22%, and 35% of senior management departed. Realized synergies totaled $19 million—42% of projections. The acquisition destroyed approximately $180 million in shareholder value.

Company B acquired a $280 million revenue target for $385 million (6.9x revenue, 13.5x EBITDA), projecting $38 million in annual synergies. The acquirer conducted 14 weeks of comprehensive due diligence including operational, cultural, and customer dimensions. A clean team developed a detailed integration blueprint pre-close. The integration strategy preserved the target's brand and go-to-market approach while integrating back-office functions. Cultural workshops aligned leadership teams. Customer communication emphasized continuity. After 24 months, revenue grew 12%, customer attrition was 5%, and key talent retention exceeded 90%. Realized synergies reached $41 million—108% of projections. The acquisition created approximately $240 million in shareholder value.

The difference? Company B invested an additional $2.3 million in due diligence and integration planning—generating a 100x return on that incremental investment through superior execution.

09 The Path Forward: Integration as Competitive Advantage

As M&A activity continues its recovery trajectory into 2025-2026, with deal volumes projected to reach $3.6-3.8 trillion globally, integration capability increasingly differentiates serial acquirers from occasional dealmakers. Organizations that develop institutional integration competence—documented playbooks, experienced integration teams, proven methodologies, and sophisticated tracking systems—generate sustainable competitive advantages in acquiring and integrating targets.

This capability building requires investment. Leading acquirers maintain dedicated corporate development and integration functions, conduct post-mortems on every transaction (successful and failed), and continuously refine methodologies. Some establish "integration academies" that train managers in integration leadership, creating a bench of integration-capable leaders.

The role of technology in supporting integration continues to expand. Purpose-built integration management platforms enable workstream tracking, synergy monitoring, and stakeholder communication. Advanced analytics identify integration risks through pattern recognition across multiple deals. AI-enabled tools accelerate due diligence by rapidly analyzing contracts, customer agreements, and operational data.

The fundamental truth remains unchanged: M&A success is determined not in the boardroom where deals are approved, but in the conference rooms, warehouses, and customer meetings where integration occurs.

10 Conclusion: From Value Destruction to Value Creation

The persistence of M&A failure rates—60-70% of deals failing to create value—represents both a challenge and an opportunity. Organizations that master post-merger integration can generate extraordinary returns in an environment where most acquirers stumble. The path forward requires acknowledging that integration is not an afterthought but the primary determinant of deal success.

This begins with comprehensive due diligence that extends beyond financial validation to assess operational feasibility, cultural compatibility, and integration complexity. It continues with detailed integration planning that begins pre-close, establishes clear governance, and maintains rigorous tracking. It demands adequate resourcing, executive commitment, and organizational discipline to execute methodically over 18-36 months.

Most critically, it requires humility—recognizing that combining two organizations is profoundly difficult, that unexpected challenges will emerge, and that flexibility and adaptability matter as much as planning. The acquirers that approach integration with appropriate respect for its complexity, invest in capability building, and learn from both successes and failures will increasingly separate themselves from the pack.

For CFOs, corporate development leaders, and M&A advisors navigating this landscape, the imperative is clear: integration capability is no longer optional but essential. The tools and platforms available today, including solutions like iValuate, enable more sophisticated analysis during due diligence and more rigorous tracking during integration. Combined with experienced leadership, proven methodologies, and organizational commitment, these capabilities transform M&A from a value destruction lottery into a systematic value creation engine. In an era where inorganic growth remains essential for competitive positioning, mastering post-merger integration is not merely advantageous—it is existential.