Table of Contents9 sections

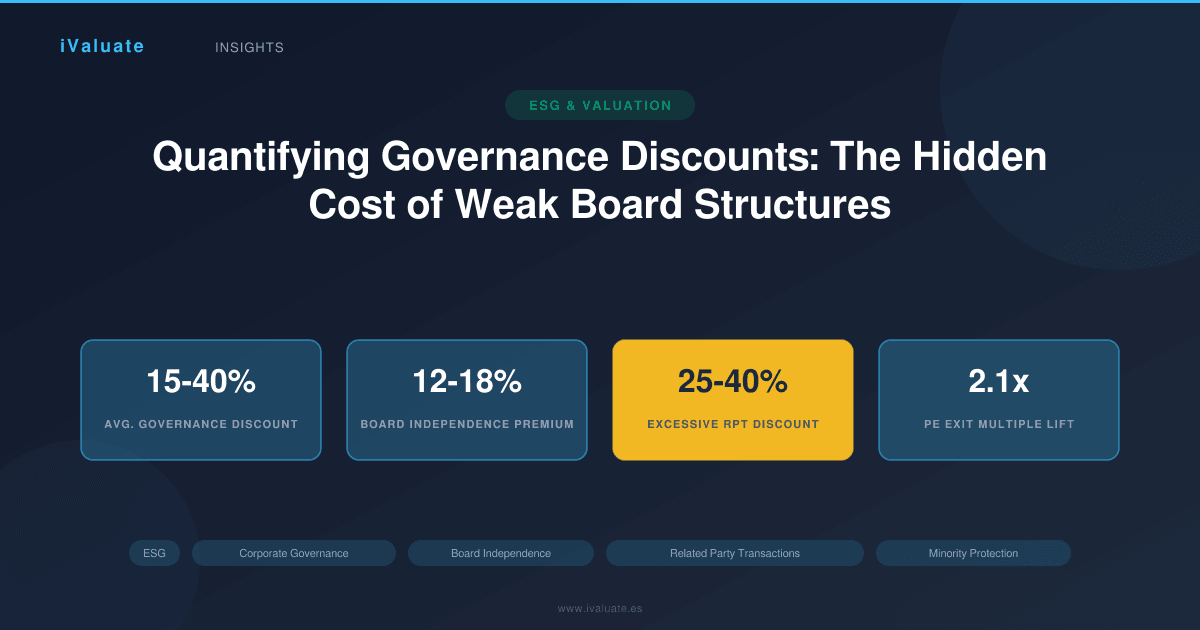

In the evolving landscape of corporate valuation, governance quality has emerged as a critical value driver that can no longer be relegated to qualitative footnotes. As institutional investors increasingly integrate ESG criteria into their investment frameworks, the financial impact of governance deficiencies has become quantifiable, measurable, and material. Companies with weak board structures, inadequate minority protections, and problematic related party transactions now face systematic valuation discounts that can range from 15% to 40% depending on jurisdiction and severity.

The governance premium—or conversely, the governance discount—represents the differential in valuation multiples between well-governed and poorly-governed companies with otherwise comparable financial profiles. This phenomenon has intensified in 2025-2026 as regulatory scrutiny has heightened following several high-profile governance failures in emerging markets and as passive investment vehicles have adopted more stringent governance screens.

01 The Empirical Foundation: Measuring Governance Impact on Value

Quantifying governance quality requires a systematic framework that translates qualitative board characteristics into measurable value adjustments. Academic research and practitioner studies have consistently demonstrated that governance deficiencies create agency costs, increase cost of capital, and ultimately compress valuation multiples.

A comprehensive 2024 study analyzing over 3,200 publicly traded companies across 42 jurisdictions found that firms in the bottom quartile of governance scores traded at an average discount of 23% to their top-quartile peers when controlling for industry, size, profitability, and growth. This discount manifested across multiple valuation metrics:

- Price-to-earnings multiples: 18-25% lower for weak governance companies

- EV/EBITDA multiples: 15-22% compression

- Price-to-book ratios: 28-35% discount, particularly pronounced in emerging markets

- Tobin's Q: 0.31 points lower on average

These discounts are not merely statistical artifacts but reflect rational investor behavior. Institutional investors systematically demand higher returns (lower entry multiples) to compensate for elevated agency risk, information asymmetry, and potential expropriation by controlling shareholders.

Board Independence: The Primary Value Driver

Board independence stands as the single most significant governance factor affecting valuation. The composition, expertise, and true independence of a company's board directly influences investor confidence and willingness to pay premium multiples.

Current market data from 2025 indicates that companies with majority-independent boards (defined as boards where at least 50% of directors have no material relationship with management or controlling shareholders) command a governance premium averaging 12-18% compared to boards dominated by insiders or affiliated directors. This premium increases to 20-28% when boards feature:

- Fully independent audit committees with financial expertise

- Independent compensation committees with no interlocking directorships

- Separation of CEO and Chairman roles

- Regular executive sessions without management present

- Robust director evaluation and refreshment processes

The valuation impact becomes particularly acute in family-controlled businesses and emerging market companies where board independence is often nominal rather than substantive. A 2025 analysis of Southeast Asian conglomerates revealed that companies with boards featuring three or more truly independent directors (verified through network analysis and transaction history) traded at EV/EBITDA multiples 4.2x higher than peers with purely ceremonial independent directors.

True board independence extends beyond formal designations to encompass economic independence, social independence, and demonstrated willingness to challenge management decisions. Valuation professionals must look beyond board composition disclosures to assess actual governance effectiveness.

02 Related Party Transactions: Quantifying Expropriation Risk

Related party transactions (RPTs) represent one of the most direct mechanisms through which controlling shareholders can extract value from minority investors. The prevalence, materiality, and disclosure quality of RPTs serve as critical inputs in governance-adjusted valuation models.

In jurisdictions with weak minority protections, excessive or opaque related party transactions can justify valuation discounts of 25-40%. The quantification methodology typically involves:

RPT Materiality Assessment

Valuation professionals should calculate RPT intensity ratios to benchmark against industry norms:

- RPT Revenue Ratio: Related party revenues / Total revenues

- RPT Asset Ratio: Related party receivables / Total assets

- RPT Purchase Ratio: Related party purchases / Cost of goods sold

- RPT Financing Ratio: Related party loans / Total debt

Companies exceeding industry median RPT ratios by more than 50% typically warrant initial discount considerations of 10-15%, with adjustments based on transaction transparency and fairness opinions.

Transaction Quality and Disclosure

Not all related party transactions destroy value. The critical distinction lies in whether RPTs occur on arm's-length terms with appropriate disclosure and independent approval. A practical scoring framework assesses:

- Independent director approval (pre-transaction): Reduces discount by 3-5%

- Independent fairness opinions: Reduces discount by 4-7%

- Detailed disclosure of terms and rationale: Reduces discount by 2-4%

- Minority shareholder approval for material RPTs: Reduces discount by 5-8%

- Regular third-party audits of RPT pricing: Reduces discount by 3-5%

Conversely, red flags that amplify governance discounts include:

- RPTs disclosed only in footnotes with minimal detail: Additional 5-8% discount

- Patterns of asset transfers to related entities below market value: Additional 10-15% discount

- Loans to related parties on non-commercial terms: Additional 8-12% discount

- Management services agreements with controlling shareholder entities lacking clear deliverables: Additional 6-10% discount

Case Example: Asian Manufacturing Conglomerate

A mid-market manufacturing company in Southeast Asia with revenues of $420 million presented for valuation in early 2025. Initial analysis suggested an EV/EBITDA multiple of 8.5x based on comparable public companies and recent M&A transactions in the sector. However, detailed governance due diligence revealed significant concerns:

- Board composition: 7 of 9 directors were family members or long-time business associates

- Related party sales: 34% of revenues derived from entities controlled by the founding family

- Asset transactions: Three significant property sales to related entities in prior 24 months at values 15-20% below independent appraisals

- Financing arrangements: $45 million in loans to related entities at below-market rates

The governance adjustment framework yielded a cumulative discount of 32%, reducing the applicable multiple to 5.8x. This translated to a valuation difference of approximately $135 million—a material impact that fundamentally altered transaction economics and required governance remediation as a condition of investment.

03 Minority Protection Mechanisms and Valuation Premiums

The strength of minority shareholder protections—both legal and structural—directly influences the magnitude of governance discounts. Companies operating in jurisdictions with robust minority rights or those that voluntarily adopt enhanced protections can substantially reduce governance-related valuation compression.

Jurisdictional Framework

The legal environment establishes the baseline for minority protection. The World Bank's Protecting Minority Investors index and similar governance metrics provide quantitative benchmarks. In 2025-2026, we observe clear valuation differentials based on jurisdictional strength:

- Strong protection jurisdictions (UK, Singapore, Hong Kong, Canada): Base governance discount of 5-10% for weak internal governance

- Moderate protection jurisdictions (Germany, Japan, South Korea): Base discount of 12-18%

- Weak protection jurisdictions (many emerging markets): Base discount of 20-30%

These base discounts can be modified substantially through company-specific governance enhancements.

Structural Protections That Command Premiums

Companies can implement specific mechanisms that demonstrably protect minority interests and thereby reduce governance discounts:

Tag-along rights: Provisions ensuring minority shareholders can participate in control transactions at the same terms as controlling shareholders reduce discounts by 4-7%. Full tag-along rights (100% participation) command higher premium adjustments than partial rights (e.g., 80% participation).

Put options and liquidity mechanisms: Structured exit rights allowing minority shareholders to sell at predetermined formulas or through periodic tender offers reduce discounts by 6-10%, depending on pricing methodology and frequency.

Supermajority voting requirements: Charter provisions requiring supermajority approval (typically 75-80%) for major decisions including M&A, significant asset sales, or charter amendments provide meaningful protection. These reduce discounts by 5-8% when genuinely enforceable.

Independent director veto rights: Governance structures granting independent directors specific veto authority over related party transactions or major strategic decisions reduce discounts by 7-11%, representing one of the most effective structural protections.

Mandatory independent fairness opinions: Requirements for independent valuation opinions on significant transactions, with results disclosed to all shareholders, reduce discounts by 3-5%.

The cumulative effect of multiple minority protection mechanisms can reduce governance discounts by 20-35%, effectively transforming a company's valuation profile and access to capital. However, these protections must be genuine and enforceable—cosmetic provisions identified during due diligence provide no valuation benefit.

04 Quantitative Governance Scoring Models

Professional valuation practice increasingly employs structured governance scoring models that translate qualitative factors into quantitative discount adjustments. A robust framework typically encompasses four dimensions:

Board Quality Score (35% weight)

- Independence percentage (10 points maximum)

- Financial expertise on audit committee (5 points)

- CEO/Chairman separation (5 points)

- Board diversity and expertise breadth (5 points)

- Director tenure and refreshment (5 points)

- Meeting frequency and attendance (5 points)

Shareholder Rights Score (30% weight)

- Voting rights alignment with economic interest (10 points)

- Tag-along and drag-along provisions (8 points)

- Supermajority requirements for major decisions (7 points)

- Preemptive rights and anti-dilution protections (5 points)

Transparency and Disclosure Score (20% weight)

- Financial reporting quality and timeliness (8 points)

- Related party transaction disclosure (7 points)

- Beneficial ownership transparency (5 points)

Related Party Transaction Management Score (15% weight)

- RPT approval processes (6 points)

- Independent fairness opinions (5 points)

- RPT materiality and arm's-length pricing (4 points)

Companies are scored on a 100-point scale, with governance discounts calibrated to score ranges:

- 80-100 points: No governance discount (potential 5-10% premium for exceptional governance)

- 60-79 points: 5-12% governance discount

- 40-59 points: 13-22% governance discount

- 20-39 points: 23-35% governance discount

- Below 20 points: 36-50% governance discount (often rendering company uninvestable for institutional capital)

05 Industry-Specific Governance Considerations

Governance materiality varies significantly across sectors, requiring calibrated approaches to discount quantification.

Financial Services

Banks, insurers, and asset managers face heightened governance scrutiny given fiduciary responsibilities and regulatory oversight. Weak governance in financial institutions typically commands 1.5-2.0x the standard discount given systemic risk implications. Board risk committee independence and expertise become paramount, with deficiencies justifying 8-12% incremental discounts.

Family-Controlled Businesses

Family businesses represent a distinct governance challenge where concentrated ownership can create both value (long-term orientation, patient capital) and destroy value (nepotism, expropriation). The governance discount for family businesses averages 18-25% but can be reduced to 5-8% through:

- Family constitutions and governance protocols

- Professional, non-family management in key roles

- Independent board majority with meaningful authority

- Transparent succession planning

Technology and High-Growth Companies

Dual-class share structures remain common in technology companies, creating inherent governance concerns. However, market acceptance varies based on founder track record and sunset provisions. Companies with dual-class structures lacking sunset clauses face 12-18% governance discounts, reduced to 4-8% with time-based or event-based conversion provisions.

06 Governance Due Diligence in M&A Contexts

In merger and acquisition transactions, governance quality assessment has evolved from checkbox compliance review to sophisticated value impact analysis. Private equity investors, in particular, have developed rigorous governance due diligence protocols given the direct impact on exit valuations.

A 2025 survey of middle-market private equity firms revealed that 78% now employ dedicated governance specialists during due diligence, up from 43% in 2022. These specialists conduct:

- Board effectiveness assessments through director interviews

- Related party transaction forensic analysis spanning 3-5 years

- Beneficial ownership mapping to identify hidden related parties

- Governance gap analysis against institutional investor expectations

- Post-acquisition governance enhancement roadmaps

The business case for governance remediation has become compelling. Private equity portfolio companies implementing comprehensive governance improvements post-acquisition achieve exit multiples averaging 2.1x higher than comparable companies maintaining weak governance structures. This translates to IRR improvements of 4-7 percentage points—material alpha in competitive markets.

07 Governance Enhancements: The Path to Premium Valuations

For companies seeking to eliminate governance discounts and potentially command governance premiums, a systematic enhancement program typically requires 18-36 months to implement and demonstrate credibility. Key initiatives include:

Board Transformation

- Recruit genuinely independent directors with relevant expertise (not ceremonial appointments)

- Implement robust committee structures with independent chairs

- Establish regular executive sessions and board evaluation processes

- Develop comprehensive director onboarding and continuing education

Related Party Transaction Reform

- Conduct comprehensive RPT audit and rationalization

- Implement independent approval requirements for all material RPTs

- Obtain fairness opinions for significant transactions

- Enhance disclosure quality with clear business rationale

Minority Protection Enhancement

- Adopt tag-along rights in shareholder agreements

- Implement supermajority voting for major decisions

- Create independent director veto rights over related party transactions

- Establish regular liquidity mechanisms for minority shareholders

Transparency and Disclosure

- Upgrade financial reporting to international standards (IFRS)

- Implement quarterly reporting even if not legally required

- Provide detailed beneficial ownership disclosure

- Conduct regular investor relations activities

The investment required for governance transformation typically ranges from $500,000 to $2 million for middle-market companies, depending on starting position and target state. This investment generates returns through multiple channels: higher valuation multiples, lower cost of capital, improved access to institutional investors, and reduced regulatory risk.

08 The Future of Governance-Adjusted Valuation

As we progress through 2025 and into 2026, several trends are amplifying the importance of governance in valuation:

Regulatory convergence: Jurisdictions worldwide are strengthening minority protection requirements and beneficial ownership transparency. Companies in emerging markets face increasing pressure to adopt developed market governance standards to access international capital.

ESG integration: The 'G' in ESG has moved from afterthought to co-equal status with environmental and social factors. Major institutional investors now employ governance scoring as a primary screening criterion, with 67% of assets under management subject to governance-based exclusions or adjustments.

Technology-enabled transparency: Blockchain-based shareholder registries, AI-powered related party transaction monitoring, and digital board portals are making governance quality more visible and verifiable, reducing information asymmetry.

Activist pressure: Governance-focused activist investors have proliferated, targeting companies with weak structures and extracting value through governance improvements rather than operational changes alone.

For valuation professionals, these trends necessitate more sophisticated governance assessment capabilities. The days of applying generic minority discounts or control premiums without detailed governance analysis have passed. Modern valuation practice requires:

- Structured governance scoring frameworks with empirical calibration

- Industry-specific governance benchmarking databases

- Forensic related party transaction analysis capabilities

- Understanding of jurisdictional legal frameworks and enforcement mechanisms

- Ability to model governance improvement scenarios and value creation paths

09 Conclusion: Governance as a Quantifiable Value Driver

The governance discount has evolved from a theoretical concept to a measurable, material factor in corporate valuation. Companies with weak board structures, problematic related party transactions, and inadequate minority protections face systematic valuation compressions of 15-40%, translating to tens or hundreds of millions in lost enterprise value for middle-market and large companies.

Conversely, companies that invest in genuine governance excellence can eliminate these discounts and potentially command premiums of 10-15% relative to peers. The business case for governance transformation is compelling: modest investments in board quality, transparency, and minority protections generate substantial returns through higher valuation multiples, lower cost of capital, and improved access to institutional investors.

For CFOs, M&A advisors, and private equity professionals, governance-adjusted valuation has become an essential capability. Transactions increasingly hinge on accurate governance risk assessment, with governance remediation often required as a condition of investment or as a value creation lever post-acquisition.

Professional valuation platforms like iValuate have responded to this evolution by incorporating governance assessment modules that enable systematic scoring, benchmarking, and discount quantification. These tools help professionals move beyond subjective governance judgments to data-driven, defensible valuation adjustments that reflect the true economic impact of governance quality. As governance continues to gain prominence in investment decision-making, the ability to accurately quantify its value impact will increasingly differentiate sophisticated valuation professionals from those applying outdated methodologies.

The message for company management is clear: governance quality is not merely a compliance obligation or reputational consideration—it is a direct driver of enterprise value that can be measured, managed, and optimized. In an era of heightened investor scrutiny and regulatory expectations, governance excellence has become a competitive advantage with quantifiable financial returns.