Table of Contents10 sections

Professional services firms represent one of the most challenging valuation assignments in corporate finance. Unlike asset-intensive businesses or product companies with tangible inventories, these organizations derive their value almost entirely from human capital—the expertise, relationships, and reputations of their professionals. As we navigate the 2025-2026 market environment, understanding the unique characteristics and valuation methodologies for law firms, consulting practices, accounting firms, and similar businesses has become increasingly critical for M&A advisors, private equity investors, and firm partners contemplating succession or growth transactions.

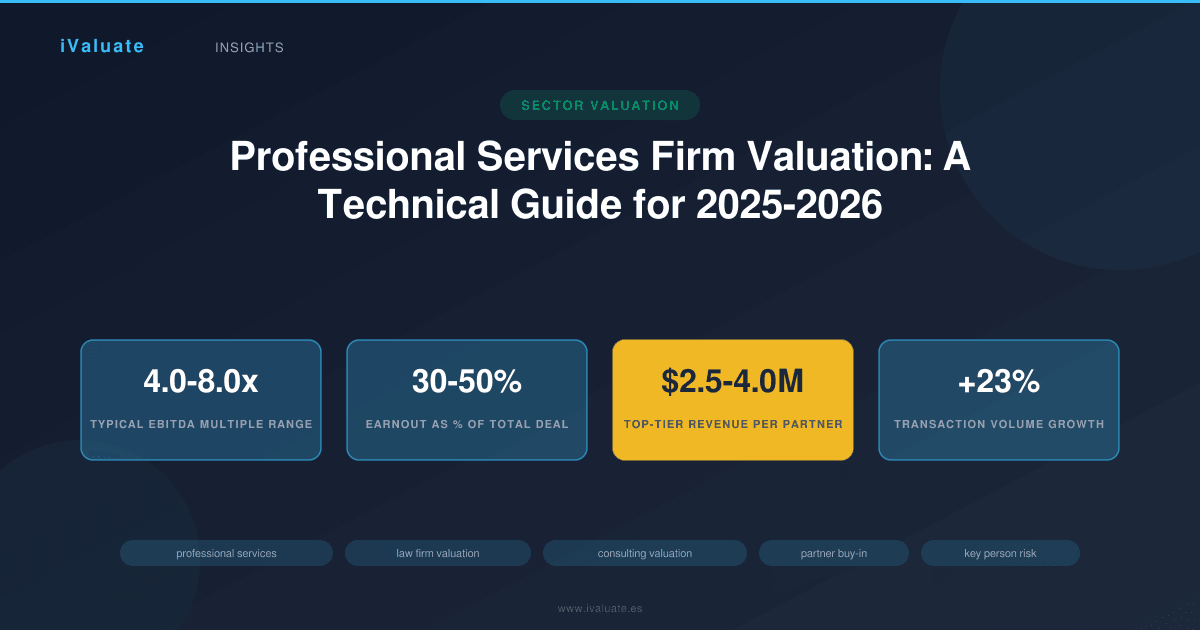

The professional services sector has experienced significant consolidation over the past three years, with transaction volumes in the legal and consulting sectors increasing by approximately 23% between 2023 and 2025. This acceleration reflects both demographic pressures—aging Baby Boomer partners seeking liquidity—and strategic imperatives as mid-sized firms pursue scale to compete with larger platforms. However, the valuation approaches that work for traditional businesses often fail to capture the economic realities of people-dependent enterprises.

01 The Fundamental Challenge: Human Capital as the Primary Asset

The central valuation challenge for professional services firms stems from a simple reality: the assets walk out the door every evening. Unlike manufacturing companies with machinery or technology firms with patents, a law firm's value resides in the minds, relationships, and reputations of its partners and senior professionals. This creates several unique valuation considerations:

- Client portability: In many professional services contexts, clients maintain relationships with individual professionals rather than the firm itself. A partner's departure can result in immediate revenue loss of 60-80% of their book of business.

- Earnings volatility: Revenue streams depend on continuous professional effort rather than recurring contracts or installed bases, creating greater year-to-year variability.

- Limited transferability: The specialized knowledge and client relationships that generate profits cannot easily be transferred to new owners without the cooperation of existing professionals.

- Partnership structures: Many professional services firms operate as partnerships rather than corporations, with complex profit-sharing arrangements and capital structures that complicate traditional valuation approaches.

These factors explain why professional services firms typically trade at lower multiples than comparable businesses in other sectors. While a software company might command 8-12x EBITDA in the current market, a consulting firm with similar profitability might trade at 4-7x EBITDA, with the discount reflecting key person risk and client concentration concerns.

02 Key Valuation Metrics for Professional Services Firms

Valuation professionals have developed specialized metrics to assess professional services businesses that go beyond traditional financial statement analysis. Understanding these metrics is essential for both buyers and sellers in this space.

Revenue Per Partner (RPP) and Revenue Per Professional

Revenue per partner serves as a primary productivity metric and valuation benchmark across professional services sectors. In 2025, top-tier management consulting firms generate $2.5-4.0 million in revenue per partner, while mid-market firms typically achieve $1.2-2.0 million. For law firms, the range is even wider: AmLaw 100 firms average $3.8-5.2 million per equity partner, while regional firms might generate $800,000-1.5 million.

Revenue per professional (including all fee-earning staff) provides additional insight into leverage ratios and operational efficiency. A healthy consulting practice typically maintains 3.5-5.0 professionals per partner, allowing partners to focus on business development and high-value client work while junior staff deliver execution. When this ratio falls below 3.0, it often signals either a lifestyle practice with limited growth potential or a firm struggling to attract and retain talent.

These metrics directly impact valuation multiples. Firms with RPP in the top quartile of their sector typically command premium valuations—often 20-35% above median multiples—because high RPP indicates strong client relationships, premium positioning, and the ability to command higher billing rates.

Client Concentration and Relationship Depth

Client concentration represents one of the most significant valuation adjustments in professional services transactions. A firm where the top five clients represent more than 40% of revenue faces substantial key person and client retention risk. Valuation discounts of 15-30% are common when concentration exceeds this threshold.

Equally important is the depth of client relationships. Firms with multi-partner client relationships—where several partners serve different needs of the same client—demonstrate lower portability risk. During due diligence, sophisticated buyers analyze not just revenue concentration but relationship concentration: how many partners have direct relationships with each major client? Are these relationships documented and transferable, or purely personal?

Realization and Collection Rates

Professional services firms typically track three revenue metrics: standard rates (published billing rates), realization rates (percentage of standard rates actually billed), and collection rates (percentage of billed amounts actually collected). The product of these rates determines effective billing rates and cash generation.

A firm with 90% realization and 95% collection rates demonstrates strong pricing discipline and client relationships, typically supporting higher valuation multiples. Conversely, firms with realization below 80% or collection below 85% face questions about pricing power, client satisfaction, and working capital management. In the current market, buyers increasingly focus on cash collections rather than accrual-basis revenue, particularly for firms with aging receivables.

Partner Compensation as a Percentage of Revenue

Partner compensation structures vary widely across professional services sectors, but the ratio of partner compensation to total revenue provides crucial insight into both profitability and sustainability. In law firms, partner compensation typically represents 35-50% of revenue, while consulting firms often run 25-40%. These percentages must be normalized during valuation to distinguish between true economic profits and discretionary partner distributions.

A critical valuation adjustment involves determining "market-rate" compensation for partners' professional services (as opposed to their return on capital). If partners in a $20 million consulting firm collectively receive $8 million in distributions but would command $5 million in market salaries for their professional work, the true economic profit is $3 million higher than reported, significantly impacting valuation.

03 Valuation Methodologies: Adapting Traditional Approaches

Income Approach: Discounted Cash Flow with Key Person Adjustments

The income approach remains the most theoretically sound valuation method for professional services firms, but it requires significant modifications from standard DCF models. The key challenge involves projecting sustainable cash flows in businesses where revenue depends on specific individuals' continued participation.

Best practice DCF models for professional services firms incorporate several unique elements:

- Probability-weighted revenue scenarios: Rather than a single revenue projection, sophisticated models develop multiple scenarios based on partner retention assumptions. For example, a base case assuming 90% partner retention, a downside case at 70%, and an upside case at 95%, each weighted by probability.

- Key person dependency adjustments: Revenue attributable to specific partners should be discounted by the probability of their departure and the expected client retention rate upon departure. If a partner generating $3 million annually has a 20% probability of leaving within three years, and 40% of their clients would likely follow, the expected value of that revenue stream is reduced accordingly.

- Higher discount rates: Professional services firms typically warrant discount rates 2-4 percentage points higher than comparable businesses in other sectors, reflecting human capital risk. While a manufacturing company might be valued at a 12% WACC, a comparable consulting firm might require 15-16%.

- Limited terminal value: Unlike businesses with durable competitive advantages, professional services firms' terminal values should be more conservative, often calculated at lower perpetuity growth rates (1-2% rather than 2.5-3%) to reflect the continuous risk of key person departure.

In a recent transaction involving a mid-market strategy consulting firm, the valuation team developed a DCF model that explicitly tracked each partner's book of business, assigned retention probabilities based on age and contract terms, and modeled the expected client attrition upon each partner's eventual departure. This granular approach revealed that while the firm reported $15 million in EBITDA, the sustainable, risk-adjusted cash flow was closer to $11 million, resulting in a valuation 25% below what a standard DCF would suggest.

Market Approach: Comparable Transactions with Structural Adjustments

The market approach provides valuable benchmarking for professional services valuations, but comparable transaction analysis requires careful attention to deal structure and earnout provisions. In 2025-2026, professional services transactions typically include significant earnout components—often 30-50% of total consideration—tied to revenue retention, partner retention, or profitability targets.

Current market multiples for professional services firms vary significantly by subsector and size:

- Management consulting firms: 5.5-8.0x EBITDA for established firms with diversified client bases; 4.0-6.0x for smaller or more concentrated practices

- Law firms: 4.0-7.0x EBITDA for profitable practices, though many transactions are structured as partner buy-ins rather than traditional acquisitions

- Accounting firms: 6.0-9.0x EBITDA, with premiums for firms offering high-margin advisory services beyond traditional compliance work

- IT consulting and implementation: 6.5-10.0x EBITDA, particularly for firms with proprietary methodologies or platform-specific expertise

- Executive search and HR consulting: 5.0-8.0x EBITDA, with significant variation based on retained vs. contingent search mix

These multiples reflect upfront cash consideration only. When earnouts are included, total deal values often reach 7-12x EBITDA, but the earnout structure effectively transfers risk to sellers by making a portion of consideration contingent on post-closing performance.

A critical adjustment in comparable analysis involves normalizing for partner compensation. Some firms pay partners modest salaries and large distributions, while others use higher salaries and smaller profit shares. To compare transactions accurately, analysts must recast EBITDA to reflect market-rate partner compensation, often adding back 20-40% to reported EBITDA for firms with below-market partner salaries.

Asset Approach: Limited Applicability but Important for Floor Values

The asset approach has limited applicability for most professional services firms because tangible assets typically represent less than 10% of enterprise value. However, it can establish a floor value for firms with significant real estate holdings, proprietary software, or valuable brand assets.

More relevant is the concept of "adjusted book value" for partnership interests, which considers not just balance sheet assets but also the partner's share of work-in-progress, unbilled receivables, and their capital account. For partner buy-in or buyout transactions, this adjusted book value often serves as the starting point for negotiations, with goodwill or blue-sky payments added based on the firm's profitability and growth prospects.

04 The Partner Buy-In Challenge: Valuing Ownership Interests

One of the most common valuation questions in professional services firms involves partner buy-in: what should a senior associate or director pay to become an equity partner? This question intersects valuation theory with partnership economics and talent retention strategy.

Traditional buy-in structures require new partners to purchase a capital interest in the firm, typically 1-3% of equity, at a price based on the firm's book value or a multiple of earnings. In 2025, typical buy-in amounts range from $150,000 to $500,000 for mid-market firms, though larger firms may require $1-2 million or more.

The valuation methodology for buy-ins typically follows one of three approaches:

Book Value Method

The simplest approach values partnership interests at a multiple of book value (partners' capital accounts). A new partner acquiring 2% of a firm with $10 million in partners' capital would pay $200,000. This method is straightforward but ignores the firm's profitability and goodwill value. It's most common in mature, stable practices where partnership is viewed primarily as a profit-sharing arrangement rather than an equity investment.

Capitalized Earnings Method

More sophisticated firms value partnership interests based on a multiple of the firm's sustainable earnings. If a firm generates $5 million in distributable profits and trades at 5x earnings in the market, total firm value is $25 million. A 2% interest would cost $500,000. This approach better reflects economic value but requires agreement on the appropriate multiple and sustainable earnings level.

Many firms use a hybrid approach: new partners pay book value for their capital interest but also make a goodwill payment based on a multiple of earnings. This structure recognizes both the firm's tangible capital and its intangible value.

Sweat Equity and Deferred Payment Structures

Recognizing that high buy-in costs can deter talented professionals from joining the partnership, many firms have moved toward more flexible structures. Common alternatives include:

- Sweat equity: New partners earn their interest over 3-5 years through reduced compensation, effectively financing the buy-in through foregone distributions

- Seller financing: The firm loans the buy-in amount to new partners, repaid from future distributions

- Phantom equity: New partners receive profit participation without actual equity ownership, avoiding the capital requirement entirely

- Two-tier partnerships: Junior partners receive profit shares without capital requirements, while senior partners hold actual equity

Each structure has different valuation implications. Phantom equity arrangements, for instance, may reduce the firm's overall value to outside buyers because they create compensation obligations without corresponding ownership rights.

05 Key Person Risk: Quantifying and Mitigating the Primary Valuation Concern

Key person risk—the possibility that departure of one or more critical professionals will materially damage the business—represents the single largest valuation concern for professional services firms. Quantifying this risk requires both qualitative assessment and quantitative modeling.

Identifying Key Persons

Key persons are typically identified through several criteria:

- Individuals responsible for more than 15% of firm revenue

- Professionals with unique technical expertise not replicated elsewhere in the firm

- Partners with exclusive relationships to major clients

- Individuals whose departure would likely trigger additional departures

In a 2024 transaction involving a 25-person consulting firm, due diligence revealed that three partners generated 68% of revenue, with limited cross-selling or relationship sharing. The buyer applied a 35% valuation discount to reflect this concentration, reducing the purchase price from $18 million to $11.7 million. The deal was restructured with significant earnouts tied to these partners' continued employment and client retention.

Quantitative Key Person Adjustments

Sophisticated valuation models quantify key person risk through scenario analysis. For each key person, the model estimates:

- Annual probability of departure (based on age, contract terms, non-compete agreements)

- Expected client retention rate upon departure (typically 20-60% for professional services)

- Time required to replace lost revenue (usually 2-4 years)

- Cost of replacement (recruiting, training, business development investment)

These factors are then incorporated into cash flow projections, typically reducing enterprise value by 10-40% depending on the severity of concentration. A firm with well-diversified client relationships and deep partner bench strength might see only a 10-15% discount, while a practice heavily dependent on 1-2 rainmakers might face 30-40% reductions.

Mitigation Strategies and Their Valuation Impact

Professional services firms can implement several strategies to reduce key person risk and support higher valuations:

- Multi-partner client teams: Ensuring that major clients work with multiple partners reduces portability risk. Firms demonstrating this structure typically command 15-25% valuation premiums.

- Long-term employment agreements: Contracts with 3-5 year terms and significant retention bonuses provide buyers with greater certainty. Each additional year of contracted key person retention typically adds 5-8% to valuation.

- Robust non-compete and non-solicitation agreements: Enforceable restrictive covenants (where legally permissible) significantly reduce key person risk. However, enforceability varies dramatically by jurisdiction and profession.

- Institutional client relationships: Firms that have successfully transitioned from personal to institutional client relationships—where clients engage the firm rather than individuals—command substantial premiums, often 30-50% above peer firms.

- Proprietary methodologies and IP: Consulting firms with documented, proprietary approaches or software tools demonstrate less dependence on individual expertise, supporting higher multiples.

A mid-market law firm in the Southwest implemented a deliberate strategy to reduce key person risk ahead of a planned sale. Over three years, the firm created multi-partner teams for all major clients, developed formal succession plans for each practice area, and implemented a two-tier partnership structure that brought younger attorneys into profit-sharing arrangements. When the firm ultimately sold in early 2025, it achieved a 6.8x EBITDA multiple—approximately 40% above the median for comparable firms—directly attributable to these risk mitigation efforts.

06 Sector-Specific Considerations

Law Firms: Partnership Economics and Regulatory Constraints

Law firm valuations face unique challenges stemming from regulatory restrictions on ownership (in most jurisdictions, only lawyers can own law firms) and the strong partnership culture in the legal profession. Traditional M&A transactions are less common than in other professional services sectors; instead, most law firm combinations take the form of mergers or partner group acquisitions.

Valuation approaches for law firms typically focus on:

- Profits per equity partner (PPEP): The primary performance metric in legal, ranging from $400,000 to $7+ million for elite firms

- Origination credit systems: Understanding which partners originate business versus service it is critical for assessing portability risk

- Practice area mix: Transactional practices (M&A, corporate) typically command higher multiples than litigation due to more predictable revenue streams

- Leverage ratios: The ratio of associates and staff to partners affects both profitability and scalability

Law firm transactions in 2025-2026 have increasingly involved private equity-backed platforms acquiring mid-market firms, with typical structures involving upfront payments of 3-5x EBITDA plus earnouts that can double total consideration over 5-7 years. These deals often include significant rollover equity, with selling partners retaining 20-40% ownership in the combined entity.

Management Consulting: Methodology and Sector Expertise as Value Drivers

Management consulting firms range from generalist strategy practices to specialized operational or technology consultancies. Valuation multiples correlate strongly with several factors:

- Proprietary methodologies: Firms with documented, branded approaches (e.g., specific transformation frameworks, assessment tools) command 20-30% premiums

- Sector specialization: Deep expertise in high-growth sectors (healthcare, technology, financial services) supports higher multiples than generalist practices

- Recurring revenue: Consulting firms with retainer relationships or managed services components trade at significant premiums to project-based practices

- Leverage and scalability: Firms demonstrating ability to grow revenue without proportional partner additions command premium valuations

The consulting sector has seen robust M&A activity in 2024-2025, with strategic buyers (larger consulting platforms) and private equity both active. Strategic buyers typically pay higher multiples—often 7-10x EBITDA—because they can realize synergies through cross-selling and shared infrastructure. Financial buyers generally pay 5-7x EBITDA but structure deals with substantial earnouts.

Accounting Firms: The Advisory Services Premium

Accounting firm valuations increasingly reflect the mix between traditional compliance services (audit, tax, bookkeeping) and higher-margin advisory work (M&A advisory, valuation services, technology consulting). Firms with 40%+ of revenue from advisory services command multiples 30-50% higher than pure compliance practices.

The accounting sector has experienced significant consolidation, with private equity-backed platforms aggressively acquiring regional firms. Current market multiples range from 6-9x EBITDA, with the highest multiples reserved for firms demonstrating:

- Strong recurring revenue from audit and tax clients

- Growing advisory practices with differentiated capabilities

- Modern technology infrastructure and cloud-based service delivery

- Younger partner demographics reducing near-term succession risk

07 Transaction Structures: Aligning Incentives and Managing Risk

Professional services transactions rarely involve simple cash-at-closing structures. Instead, deals typically incorporate multiple components designed to align buyer and seller interests while managing key person and client retention risks.

Earnout Provisions

Earnouts in professional services deals typically represent 30-50% of total consideration and extend 3-5 years post-closing. Common earnout structures include:

- Revenue-based earnouts: Payments tied to maintaining or growing revenue, often with specific client retention thresholds

- EBITDA-based earnouts: Payments contingent on achieving profitability targets, though these can create conflicts over expense allocation

- Partner retention earnouts: Specific payments triggered by key partners remaining with the firm for defined periods

- Client retention earnouts: Payments based on retaining specific percentages of the client base

Well-structured earnouts align incentives by ensuring sellers remain motivated to support client transitions and business continuity. However, poorly designed earnouts create conflicts, particularly around investment decisions, expense allocation, and resource priorities.

Rollover Equity

Increasingly common in professional services transactions, rollover equity requires selling partners to retain 20-40% ownership in the post-transaction entity. This structure accomplishes several objectives:

- Reduces upfront cash requirements for buyers

- Ensures sellers remain committed to long-term success

- Provides sellers with potential upside from future growth or subsequent exit

- Demonstrates seller confidence in the combined entity's prospects

From a valuation perspective, rollover equity effectively transfers some risk from buyer to seller, potentially supporting higher headline valuations while reducing actual cash consideration.

Employment Agreements and Non-Competes

Virtually all professional services transactions require key partners to enter long-term employment agreements (typically 3-5 years) with defined compensation, responsibilities, and restrictive covenants. These agreements are often valued separately from the business purchase, with a portion of total consideration allocated to employment contracts for tax purposes.

The enforceability of non-compete agreements varies significantly by jurisdiction and profession. In states with strong non-compete enforcement (such as Florida or Texas), these provisions meaningfully reduce key person risk and support higher valuations. In jurisdictions with limited enforceability (California, for example), buyers must rely more heavily on earnouts and retention incentives.

08 Due Diligence Priorities for Professional Services Acquisitions

Due diligence for professional services transactions focuses heavily on areas that don't receive comparable attention in other sectors:

Client Relationship Mapping

Sophisticated buyers conduct detailed client relationship analysis, mapping which partners have relationships with each client, the depth and duration of those relationships, and the client's engagement with the firm versus individuals. This analysis often reveals concentration risks not apparent from revenue reports alone.

Partner Compensation and Economics

Understanding partner compensation structures, profit allocation formulas, and individual partner economics is essential for projecting post-transaction profitability. Buyers analyze:

- Compensation per partner relative to their production

- Profit allocation methodologies (eat-what-you-kill vs. lockstep vs. hybrid)

- Capital account balances and withdrawal rights

- Deferred compensation or retirement obligations

Pipeline and Backlog Analysis

Unlike product businesses with order backlogs, professional services firms often have less formal pipeline tracking. Due diligence should assess:

- Contracted but not yet delivered work (true backlog)

- Proposed engagements with high probability of conversion

- Recurring vs. one-time project revenue mix

- Historical win rates and pipeline conversion metrics

Talent Retention and Succession

The quality and stability of the professional team below the partner level significantly impacts value. Buyers examine:

09 Current Market Dynamics and Future Outlook

The professional services M&A market in 2025-2026 is characterized by several notable trends that impact valuations:

Private equity consolidation continues: PE-backed platforms have become dominant buyers in most professional services sectors, bringing disciplined valuation approaches and sophisticated deal structures. These platforms typically pursue roll-up strategies, acquiring multiple firms to build scale and diversification before eventual exit.

Technology integration drives premiums: Firms demonstrating effective use of AI, automation, and digital delivery platforms command significant valuation premiums. A consulting firm with proprietary technology tools might trade at 8-10x EBITDA versus 5-6x for a comparable traditional practice.

Generational transition accelerates: With Baby Boomer partners increasingly seeking liquidity, succession-driven transactions have become more common. However, younger partners often lack capital to buy out retiring partners at market valuations, creating opportunities for external buyers.

Specialization premiums expand: Generalist practices face increasing pressure, while firms with deep expertise in specific industries or service areas command premium multiples. The valuation gap between specialized and generalist firms has widened to 30-40% in many sectors.

Regulatory scrutiny increases: Particularly in accounting and legal services, regulators are paying closer attention to private equity ownership structures and potential conflicts of interest, potentially impacting future transaction structures and valuations.

10 Conclusion: Navigating Complexity in Professional Services Valuation

Valuing professional services firms requires a nuanced understanding of human capital economics, partnership structures, and the unique risks inherent in people-dependent businesses. While traditional valuation methodologies provide a framework, they must be substantially adapted to reflect key person risk, client portability, and the intangible nature of professional services assets.

The most successful transactions in this sector share several characteristics: thorough due diligence focused on relationship mapping and talent assessment, creative deal structures that align incentives through earnouts and rollover equity, and realistic expectations about valuation multiples given the inherent risks. Buyers who understand these dynamics and structure deals appropriately can build valuable platforms through strategic acquisitions. Sellers who invest in reducing key person risk, diversifying client relationships, and building institutional capabilities position themselves for premium valuations.

As the professional services sector continues to consolidate and evolve, the importance of rigorous, specialized valuation analysis only increases. Whether you're a partner contemplating a sale, a buyer evaluating acquisition opportunities, or an advisor structuring transactions, understanding the unique economics and valuation considerations of professional services firms is essential for successful outcomes.

For professionals navigating these complex valuation challenges, sophisticated analytical tools have become increasingly important. Platforms like iValuate enable advisors and business owners to efficiently model the specialized metrics, risk adjustments, and scenario analyses that professional services valuations demand, helping translate complex partnership economics into clear valuation conclusions that support informed decision-making.