Table of Contents9 sections

Management buyouts (MBOs) represent one of the most complex transaction structures in corporate finance, where the very individuals responsible for operating a business seek to acquire ownership from existing shareholders. In 2025-2026, MBO activity has surged as private equity sponsors partner with management teams to capitalize on market dislocations and attractive financing conditions. However, these transactions present distinctive valuation challenges that demand rigorous analysis and robust governance frameworks.

The fundamental tension in any MBO stems from information asymmetry: management possesses intimate knowledge of the business's operations, prospects, and risks—knowledge that outside shareholders and board members may lack. This creates a potential conflict of interest that requires careful navigation through independent valuation analysis, fairness opinions, and structured negotiation processes.

01 The MBO Landscape in 2025-2026

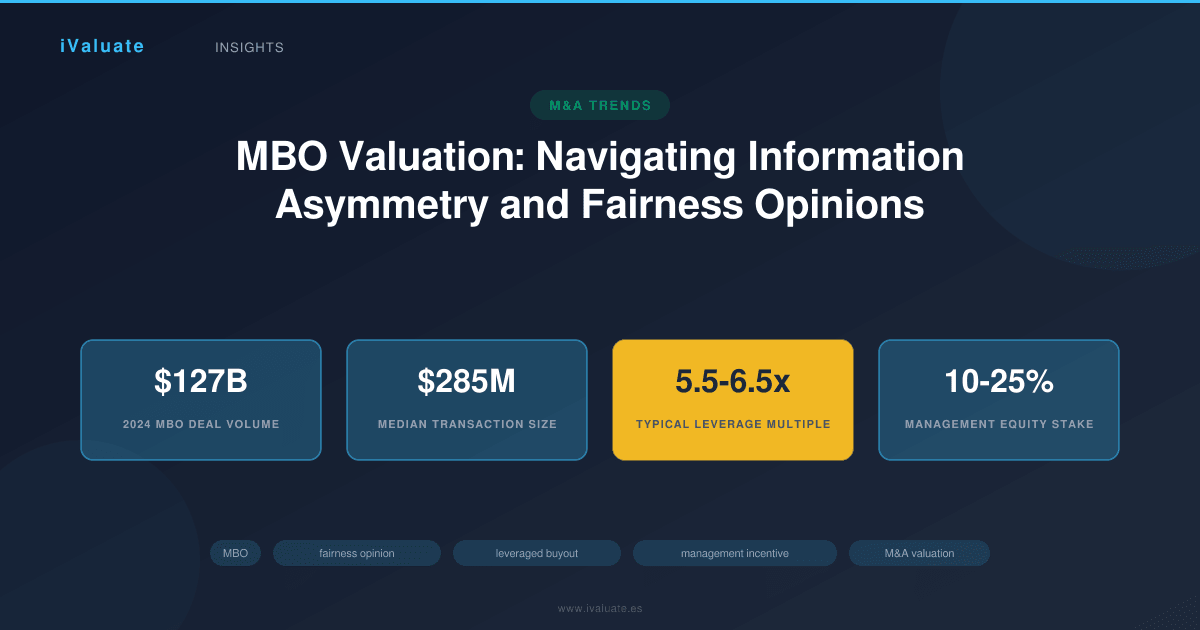

Management buyouts have experienced a notable resurgence following the market volatility of 2022-2023. According to recent data from Pitchbook and Preqin, MBO transactions in North America and Europe reached approximately $127 billion in aggregate value during 2024, representing a 23% increase from the prior year. This momentum has continued into 2025, driven by several factors:

- Attractive leverage markets: With interest rates stabilizing and debt markets reopening, leveraged buyout (LBO) financing has become more accessible, with typical senior debt multiples of 4.5-5.5x EBITDA and total leverage reaching 5.5-6.5x for quality businesses

- Founder succession needs: An aging demographic of business owners seeks liquidity while maintaining operational continuity through trusted management teams

- Private equity partnership models: Institutional sponsors increasingly view management partnerships as lower-risk entry points, particularly in middle-market transactions

- Public-to-private opportunities: Persistent valuation discounts in public markets have created attractive MBO opportunities for undervalued companies

The median MBO transaction size in 2025 stands at approximately $285 million enterprise value, with the middle market (transactions between $100 million and $1 billion) representing the most active segment. Management teams typically retain 10-25% equity ownership post-transaction, with private equity sponsors providing the majority of equity capital alongside debt financing.

02 Core Valuation Challenges in Management Buyouts

Information Asymmetry and the Knowledge Advantage

The most significant valuation challenge in MBOs stems from the inherent information asymmetry between management and other stakeholders. Management teams possess detailed knowledge of:

- Operational inefficiencies and improvement opportunities not yet reflected in financial performance

- Customer concentration risks, contract renewal probabilities, and relationship dynamics

- Pending competitive threats or market shifts not yet visible to outside observers

- Working capital optimization opportunities and hidden balance sheet strengths or weaknesses

- Key employee retention risks and organizational capability gaps

This knowledge advantage creates what economists term a "lemons problem"—outside shareholders cannot distinguish whether management's buyout offer reflects fair value or opportunistic timing. Research by Kaplan and Strömberg analyzing over 300 MBO transactions found that management teams achieved average returns of 35-40% above their initial equity investment over a 4-5 year holding period, suggesting that buyout prices often undervalued true business potential.

In a 2024 case involving a $420 million MBO of a specialty manufacturing company, the initial management offer of 8.2x EBITDA was ultimately increased to 9.7x following a competitive auction process overseen by a special committee—an 18% increase that highlighted the initial offer's inadequacy.

Projection Bias and Forecast Manipulation

Management teams preparing for MBOs face conflicting incentives when developing financial projections that underpin valuation analysis. Conservative projections support lower valuations and acquisition prices, while aggressive projections may be necessary to secure debt financing and demonstrate viable returns to equity sponsors.

This creates several valuation complications:

- Baseline suppression: Management may present conservative "base case" projections to the board while sharing more optimistic scenarios with financing sources

- Timing manipulation: Discretionary expenses may be accelerated or deferred to influence EBITDA in the valuation period

- Strategic initiative delays: Value-creating initiatives may be postponed until after the transaction closes, depressing current valuations

- Working capital management: Temporary working capital builds or releases can distort normalized cash flow analyses

Sophisticated valuation advisors address these risks through independent due diligence, third-party market research, customer interviews, and detailed variance analysis comparing management projections to historical accuracy. In complex situations, special committees may retain operational consultants to develop independent business plans and financial forecasts.

Valuation Methodology Selection and Application

MBO valuations typically employ multiple methodologies to triangulate fair value ranges:

Discounted Cash Flow (DCF) Analysis: DCF models in MBO contexts require careful consideration of discount rate selection. The weighted average cost of capital (WACC) must reflect the post-transaction capital structure, which typically involves significantly higher leverage than the pre-MBO structure. In 2025, typical MBO WACC calculations range from 10-14% for middle-market companies, depending on business risk profile and leverage levels. Terminal value assumptions warrant particular scrutiny, as management may have insights into long-term competitive positioning not available to outside analysts.

Comparable Company Analysis: Public company comparables provide market-based valuation benchmarks, though adjustments are necessary for size, growth profile, and the control premium inherent in MBO transactions. As of early 2025, median EV/EBITDA multiples for middle-market companies range from 8.5x to 12.5x depending on sector, with software and healthcare services commanding premium valuations while traditional manufacturing and distribution trade at the lower end.

Precedent Transaction Analysis: Recent MBO transactions in similar industries provide relevant benchmarks, though transaction-specific factors (strategic buyer involvement, auction competitiveness, market timing) require careful consideration. Control premiums in MBO transactions typically range from 25-35% above pre-announcement trading prices for public companies, though this varies significantly based on pre-deal valuation levels.

Leveraged Buyout Model: The LBO model works backward from target equity returns (typically 20-25% IRR for private equity sponsors) to determine supportable purchase prices. This methodology explicitly incorporates the financing structure and management incentive arrangements, providing insight into the economic feasibility of proposed transactions. However, LBO-derived valuations represent what a financial buyer can afford to pay rather than intrinsic business value, creating potential gaps with shareholder value expectations.

03 The Critical Role of Fairness Opinions

Fairness opinions have become virtually mandatory in MBO transactions, serving both substantive analytical and procedural protection functions. These opinions, typically rendered by independent investment banks or valuation firms, opine on whether the consideration offered to shareholders is fair from a financial point of view.

Fairness Opinion Standards and Methodology

A comprehensive fairness opinion in an MBO context includes:

- Multiple valuation methodologies applied independently, with appropriate weighting based on business characteristics and data availability

- Detailed analysis of management projections, including sensitivity analysis and comparison to historical performance

- Consideration of premiums paid in comparable transactions and control premium studies

- Assessment of alternative transaction structures and strategic alternatives

- Analysis of the proposed management incentive structure and its impact on shareholder value

- Review of the process followed by the special committee or board in evaluating the transaction

The opinion provider must maintain strict independence from both management and the acquiring entity. Fees are typically structured as fixed amounts rather than contingent on transaction completion, and the provider should have no material business relationships with the parties that could compromise objectivity.

In a notable 2024 Delaware Chancery Court decision involving an MBO of a retail services company, the court scrutinized the fairness opinion process extensively, ultimately finding that the opinion provider's limited scope of work and reliance on management projections without independent verification undermined its credibility.

Valuation Ranges and the "Fairness" Determination

Fairness opinions do not opine on the "best" price or optimal value—they assess whether the offered consideration falls within a range of fair values. This creates analytical challenges:

The typical fairness opinion presents valuation ranges from multiple methodologies that may span 20-30% from low to high. For example, a fairness opinion might conclude that fair value ranges from $45-58 per share across methodologies, with the offered price of $52 per share falling comfortably within this range. However, shareholders receiving $52 when the high end suggests $58 may question whether the transaction truly maximizes value.

Best practices in fairness opinion delivery include:

- Clear explanation of methodology weighting rationale and why certain approaches receive greater emphasis

- Transparency regarding key assumptions and their sensitivity impact on conclusions

- Discussion of valuation methodology limitations and factors not readily quantifiable

- Comparison of the offered premium to market benchmarks and historical trading ranges

- Analysis of the certainty of value versus potential risks of alternative paths

04 Management Incentive Structures and Valuation Impact

The design of management's post-transaction equity participation significantly impacts both deal economics and valuation considerations. Typical MBO structures provide management with:

- Rollover equity: Management invests a portion of their existing equity (or cash proceeds) into the new entity, typically at the same per-share price as other selling shareholders

- Management incentive plans: Additional equity grants, often in the form of stock options or restricted stock with time and performance vesting, representing 5-15% of post-transaction equity

- Co-investment rights: Opportunities to invest additional personal capital alongside the private equity sponsor, often at favorable terms

These arrangements create several valuation considerations:

Alignment versus enrichment: While incentive equity aligns management with value creation, excessive grants at artificially low valuations may constitute a wealth transfer from selling shareholders. Courts and regulators scrutinize situations where management receives equity at significant discounts to the price paid for other shares.

Dilution impact: Management equity grants dilute other shareholders' interests in future value creation. Fairness opinions must consider whether the transaction price adequately compensates for this dilution, particularly when management's percentage ownership increases substantially.

Ratchet provisions: Some MBO structures include ratchet mechanisms that increase management's equity percentage if certain return thresholds are achieved. While these can provide powerful incentives, they may also signal that the initial valuation was conservative relative to realistic potential.

Case Study: Technology Services MBO

In a 2024 MBO of a business services technology company, management partnered with a private equity sponsor to acquire the company from its founding family shareholders at an enterprise value of $680 million, representing 10.2x LTM EBITDA. The transaction structure included:

- Management rollover of 18% equity at the transaction price

- Additional management incentive pool of 12% with 4-year vesting

- Total management ownership of 30% post-transaction

- Private equity sponsor equity of 70%

- Debt financing of 5.8x EBITDA

The special committee's fairness opinion provider analyzed whether the 10.2x multiple adequately reflected fair value given that management's ownership would increase from 15% to 30%. The analysis concluded that:

- The multiple represented a 15% premium to comparable public companies but was at the lower end of recent private market transactions

- Management's increased ownership was justified by their co-investment of personal capital and acceptance of significant unvested incentive equity

- The transaction price implied a 28% premium to the company's estimated standalone value under family ownership, given limited growth investment

The transaction closed successfully, though not without shareholder litigation that was ultimately dismissed based on the robust special committee process and comprehensive fairness opinion.

05 Special Committee Processes and Governance Best Practices

Effective MBO governance requires formation of a special committee of independent directors with exclusive authority to evaluate, negotiate, and approve or reject the proposed transaction. Best practices include:

- Early formation: The special committee should be established before substantive negotiations begin, ideally upon first indication of management's interest

- Exclusive authority: The committee must have clear authority to retain independent advisors, control the process timeline, and reject the transaction without full board override

- Independent advisors: The committee should retain its own financial advisor (separate from any advisor to management or the buyer group) and legal counsel with expertise in conflict transactions

- Process control: The committee should consider alternative transactions, including potential sales to third parties, to establish that the MBO represents the best available outcome

- Negotiation leverage: The committee must be willing to reject inadequate offers and push for improved terms, demonstrating genuine arm's-length negotiation

In 2025, special committees increasingly employ "market check" processes, either through pre-signing "go-shop" periods or post-signing solicitation of alternative bids. While these processes add time and complexity, they provide powerful evidence that the transaction price reflects competitive market dynamics rather than information asymmetry exploitation.

06 Regulatory and Legal Considerations

MBO transactions face heightened scrutiny from both securities regulators and shareholder litigation. Key legal considerations include:

Fiduciary Duty Standards

Directors and management involved in MBOs must navigate complex fiduciary obligations. In Delaware (the most influential corporate law jurisdiction), courts apply "entire fairness" review to conflict transactions unless certain procedural protections are implemented. The Kahn v. M&F Worldwide decision established that business judgment rule deference can be achieved through:

- Approval by a fully-empowered special committee of independent directors, AND

- Approval by a majority of disinterested shareholders (majority-of-minority vote)

These dual protections have become standard in public company MBOs, though private company transactions often rely solely on special committee processes.

Disclosure Obligations

MBO proxy statements or information statements must provide extensive disclosure regarding:

- Management's role in the transaction and any conflicts of interest

- The background and process leading to the transaction

- Financial projections and the bases for valuation analyses

- Management's post-transaction compensation and equity arrangements

- Alternative transactions considered and reasons for their rejection

- The fairness opinion and its underlying assumptions and methodologies

Inadequate disclosure, particularly regarding management projections or alternative transaction opportunities, frequently forms the basis for shareholder litigation challenging MBO transactions.

07 Leveraged Buyout Financing and Valuation Constraints

The availability and terms of debt financing significantly impact achievable MBO valuations. In the current market environment (2025-2026), typical financing structures include:

- Senior secured debt: 4.0-5.0x EBITDA at interest rates of SOFR + 350-450 basis points

- Second lien or subordinated debt: 1.0-1.5x EBITDA at SOFR + 650-850 basis points

- Equity contribution: 35-45% of total transaction value

These financing parameters create natural constraints on supportable purchase prices. A company generating $50 million EBITDA might support $250-275 million of debt, requiring $150-200 million of equity for a total enterprise value of $400-475 million, or 8.0-9.5x EBITDA.

Lenders impose financial covenants that restrict operational flexibility and require maintenance of specified leverage ratios (typically maximum total leverage of 6.0-6.5x stepping down over time) and minimum interest coverage (usually 2.0-2.5x). These constraints must be modeled in valuation analyses to ensure the business can operate successfully under the post-MBO capital structure.

08 Sector-Specific Valuation Considerations

Different industries present unique MBO valuation challenges:

Technology and Software: High growth rates and recurring revenue models support premium valuations (12-18x EBITDA in 2025), but management may have superior insight into customer churn risks, product development timelines, and competitive threats. Valuation analyses must carefully assess the sustainability of growth rates and the investment required to maintain competitive positioning.

Healthcare Services: Regulatory risks, reimbursement rate changes, and customer concentration (particularly in government-payer-dependent businesses) create valuation complexity. Management's relationships with referral sources and understanding of regulatory trends provide significant information advantages.

Manufacturing and Distribution: These businesses typically trade at 6-10x EBITDA, with valuation heavily dependent on customer diversification, competitive positioning, and capital intensity. Management may have unique insight into customer relationship strength and competitive win/loss dynamics not visible in financial statements.

09 The Path Forward: Ensuring Fair Value in MBO Transactions

As MBO activity continues its strong trajectory through 2025 and 2026, market participants must remain vigilant in addressing information asymmetry and ensuring robust valuation processes. Several trends are emerging:

- Enhanced data analytics: Advanced analytics tools enable independent advisors to conduct more sophisticated analysis of customer behavior, competitive positioning, and operational efficiency, reducing reliance on management-provided information

- Expanded market checks: Special committees increasingly insist on broad solicitation of alternative bidders to establish competitive market dynamics

- Structured auctions: Rather than negotiated transactions, some companies are conducting formal auction processes even when management is a bidder, ensuring price discovery through competition

- Earnout provisions: When valuation gaps exist between management's view of potential and special committee assessments, earnout provisions can bridge differences while protecting shareholders' interests in upside realization

The sophistication of valuation tools and analytical approaches continues to advance, enabling more rigorous assessment of fair value even in the face of information asymmetry. Professional platforms like iValuate provide institutional-quality valuation capabilities that special committees and their advisors can leverage to conduct independent analyses, stress-test management projections, and benchmark proposed transaction terms against market standards.

The key to successful MBO execution lies not in eliminating conflicts of interest—which are inherent to the structure—but in implementing robust processes that counterbalance information asymmetry through independent analysis, competitive dynamics, and aligned governance.

For CFOs considering MBO opportunities, the message is clear: transparency, robust process, and genuine arm's-length negotiation are not obstacles to transaction completion but rather essential elements that ensure sustainable outcomes and minimize legal risk. For board members and special committees, the availability of sophisticated analytical tools and experienced advisors means there is no excuse for inadequate valuation rigor.

As we progress through 2025-2026, the MBO market will continue to evolve, but the fundamental principles of fair value determination remain constant. Success requires balancing management's legitimate interests in ownership transition with shareholders' rights to receive fair value for their interests—a balance best achieved through independent analysis, competitive processes, and the application of rigorous valuation methodologies. Tools like iValuate help professionals navigate these complex analyses efficiently, ensuring that valuation conclusions rest on solid analytical foundations rather than information asymmetry advantages.