Table of Contents9 sections

The International Valuation Standards Council (IVSC) released its 2025 edition of the International Valuation Standards (IVS) in January 2025, marking the most substantial revision to the global valuation framework since the 2022 restructuring. These updates arrive at a critical juncture—global M&A activity rebounded 23% in 2024, ESG considerations now influence 87% of institutional investment decisions, and digital assets have achieved mainstream acceptance with total market capitalization exceeding $3.2 trillion as of Q1 2025.

For valuation professionals, these changes are not merely academic. They fundamentally alter how we approach fair value measurements, integrate non-financial factors, and document our methodologies. This article examines the key changes in IVS 2025 and their practical implications for corporate finance professionals, M&A advisors, and valuation specialists.

01 Overview of the 2025 Revision Framework

The IVSC's 2025 revision process began in mid-2023, driven by three primary catalysts: the proliferation of intangible-heavy business models, the integration of sustainability factors into investment decisions, and the emergence of digital assets as a distinct asset class. The Council conducted consultations with over 450 valuation professionals across 62 jurisdictions, resulting in amendments to five existing standards and the introduction of two new technical information papers.

The revision maintains the hierarchical structure established in 2022, with General Standards (IVS 101-105) providing overarching principles and Asset Standards (IVS 200-500) addressing specific asset classes. However, the 2025 edition introduces enhanced guidance that reflects the evolving complexity of modern valuation practice.

Key Structural Changes

- Enhanced IVS 101 (Scope of Work): Now requires explicit documentation of ESG factor consideration and climate risk assessment applicability

- Revised IVS 104 (Bases of Value): Clarifies fair value hierarchy alignment with IFRS 13 and introduces "sustainable value" as a supplementary basis

- New IVS 105 (Valuation Approaches and Methods): Consolidates guidance previously scattered across multiple standards and introduces digital asset-specific methodologies

- Expanded IVS 210 (Intangible Assets): Addresses AI-generated intellectual property, data assets, and platform ecosystems

- New Technical Information Paper on Digital Assets: Provides comprehensive guidance on cryptocurrency, NFTs, and tokenized securities

02 Critical Changes to Fair Value Measurement

The most significant practical impact for most valuers stems from enhanced guidance on fair value measurement, particularly the alignment with IFRS 13 and the integration of market participant assumptions in distressed or illiquid markets.

Market Participant Perspective Enhancement

IVS 2025 strengthens the requirement to adopt a market participant perspective when determining fair value, moving beyond the previous "willing buyer and willing seller" construct. The updated standard explicitly requires valuers to:

- Identify the principal (or most advantageous) market for the asset or liability

- Consider market participant assumptions about risk, including systematic and unsystematic factors

- Incorporate market participant views on growth prospects, even when these differ from management projections

- Document why specific market participant characteristics were selected

In practice, this creates tension when valuing private companies for financial reporting purposes. Consider a mid-market software company with $50 million in revenue and 40% EBITDA margins. Management projects 25% annual growth based on their product roadmap. However, market participants—represented by comparable public companies and recent private transactions—price similar assets at 15-18% growth expectations due to macroeconomic uncertainty and competitive pressures.

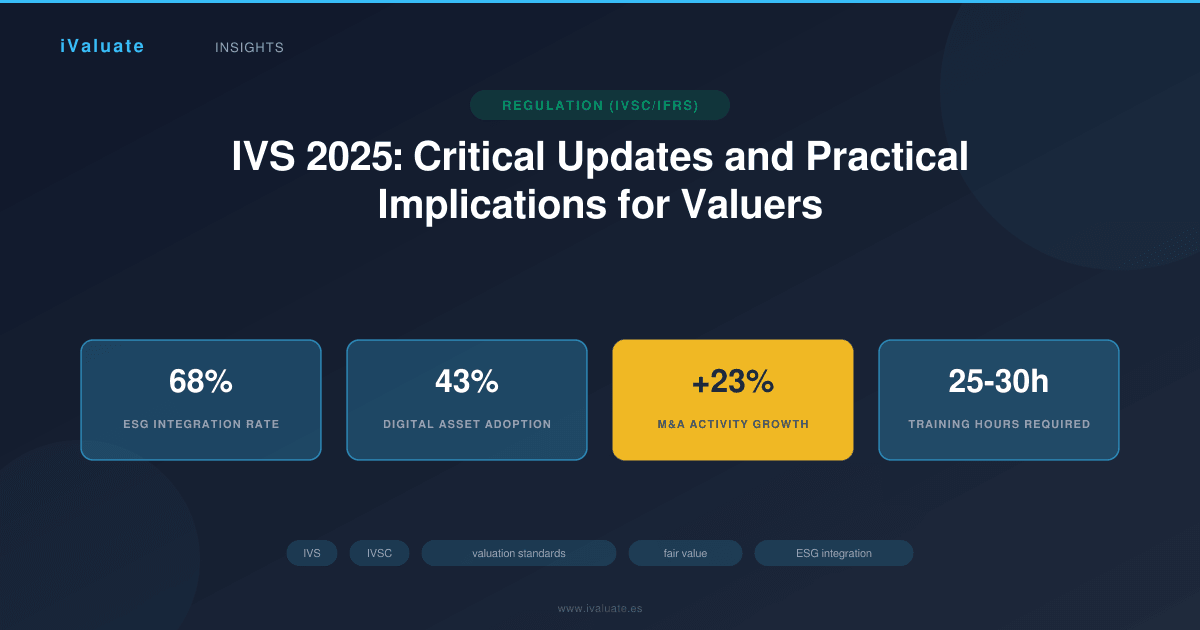

Under IVS 2025, the valuer must give primacy to market participant assumptions, potentially resulting in a lower valuation than management's internal view would suggest. This has created friction in approximately 30% of purchase price allocation engagements in early 2025, according to preliminary data from the American Society of Appraisers.

Illiquid Market Guidance

The 2025 revision provides crucial clarification for fair value measurements when markets are illiquid or distressed—a scenario that became increasingly relevant during the 2023-2024 private equity valuation challenges. IVS 104 now explicitly states that fair value assumes an orderly transaction, but orderly does not mean extended marketing periods are always appropriate.

"Fair value assumes a transaction between market participants at the measurement date under current market conditions, including conditions that exist in illiquid markets. It does not assume a forced or distressed transaction." — IVS 104.30

This distinction matters enormously for portfolio company valuations. During 2023-2024, many private equity firms faced scrutiny over whether their portfolio valuations reflected fair value when comparable public companies had declined 40-60% but private marks showed only 10-15% declines. The enhanced guidance requires valuers to distinguish between temporary illiquidity (where holding for better conditions is reasonable) and fundamental market repricing (where current conditions must be reflected).

03 ESG Integration and Climate Risk Assessment

Perhaps the most forward-looking aspect of IVS 2025 is the integration of environmental, social, and governance factors into mainstream valuation practice. This reflects the reality that ESG considerations now materially affect asset values across most sectors.

Mandatory ESG Consideration Framework

IVS 101 now requires valuers to explicitly consider whether ESG factors materially affect value and, if so, how these factors have been incorporated. This doesn't mandate ESG adjustments in every valuation, but it does require documentation of the consideration process.

The standard identifies three pathways for ESG integration:

- Cash Flow Impact: Direct effects on revenue, costs, or capital requirements (e.g., carbon pricing, regulatory compliance costs, resource efficiency)

- Risk Premium Adjustment: Effects on discount rates through systematic risk factors (e.g., stranded asset risk, transition risk, social license to operate)

- Market Multiple Effects: Valuation multiples that reflect market participant ESG preferences (e.g., premium multiples for renewable energy assets, discounts for high-emission industries)

A 2025 study by the CFA Institute found that 68% of institutional investors now incorporate ESG factors into valuation models, up from 41% in 2022. This shift is particularly pronounced in Europe, where the EU's Corporate Sustainability Reporting Directive (CSRD) requires detailed ESG disclosures from over 50,000 companies.

Climate Risk Assessment Requirements

For valuations involving long-lived assets or businesses with significant physical or transition climate risks, IVS 2025 introduces specific guidance aligned with the Task Force on Climate-related Financial Disclosures (TCFD) framework. Valuers must now consider:

- Physical risks: Asset impairment from extreme weather, sea-level rise, or temperature changes

- Transition risks: Policy changes, technological disruption, market shifts, and reputational impacts

- Scenario analysis: For assets with lives exceeding 10 years, consideration of multiple climate scenarios

This has immediate practical implications for real estate, infrastructure, and energy sector valuations. A coastal commercial property portfolio, for instance, now requires explicit consideration of flood risk under various climate scenarios, potentially affecting both cash flows (insurance costs, tenant demand) and exit multiples (buyer risk perceptions).

In one recent case, a European logistics REIT saw its valuation reduced by approximately 8% when climate risk assessment revealed that 15% of its portfolio faced elevated flood risk by 2040, increasing insurance costs by an estimated 40-60% and reducing tenant demand for affected properties.

04 Digital Assets and Intangible Asset Valuation

The explosive growth of digital assets and intangible-heavy business models necessitated substantial updates to IVS 210 and the introduction of new technical guidance.

Digital Asset Valuation Framework

The new Technical Information Paper on Digital Assets provides the first comprehensive international guidance on valuing cryptocurrencies, non-fungible tokens (NFTs), tokenized securities, and digital collectibles. This addresses a critical gap—by early 2025, institutional adoption of digital assets had reached unprecedented levels, with 43% of Fortune 500 companies holding some form of digital asset on their balance sheets.

The framework establishes three primary valuation approaches for digital assets:

- Market Approach: Using observable market prices from liquid exchanges, adjusted for liquidity, counterparty risk, and market depth

- Cost Approach: Particularly relevant for proof-of-work cryptocurrencies, considering mining costs, energy consumption, and network difficulty

- Income Approach: For yield-bearing digital assets, staking rewards, or utility tokens with cash flow generation

The guidance explicitly addresses the challenge of valuing illiquid or thinly traded digital assets. For NFTs or tokenized real-world assets without active markets, valuers must consider the underlying asset value, platform risk, smart contract functionality, and market participant liquidity preferences.

AI and Data Asset Valuation

IVS 210's expansion includes groundbreaking guidance on artificial intelligence systems and data assets—two categories that barely existed in valuation literature five years ago but now represent substantial value in modern enterprises.

For AI systems, the standard distinguishes between:

- Trained models: Valued based on replacement cost, market comparables (licensing agreements), or income generation capability

- Training data: Valued separately when proprietary and material to model performance

- AI-generated intellectual property: Requires consideration of ownership rights, regulatory environment, and commercial applicability

Data assets present unique challenges because their value is often non-rivalrous (multiple uses don't deplete the asset) and context-dependent (value varies by use case). IVS 2025 requires valuers to consider data quality, completeness, exclusivity, regulatory constraints (GDPR, CCPA), and monetization pathways.

A practical example: A healthcare technology company with 15 million patient records (properly anonymized and consented) sought valuation for financial reporting. Traditional approaches struggled because the data had never been licensed or sold. The valuation team ultimately used a hybrid approach: estimating the cost to recreate the dataset ($45 million over 7 years), then applying obsolescence factors (technological, regulatory, competitive) to arrive at a fair value of $28 million. This represented approximately 22% of the company's total enterprise value.

05 Enhanced Documentation and Disclosure Requirements

IVS 2025 significantly strengthens documentation requirements, reflecting regulatory scrutiny following several high-profile valuation controversies in 2022-2024. The enhanced requirements affect both the scope of work documentation (IVS 101) and the final valuation report (IVS 103).

Scope of Work Enhancements

The updated IVS 101 requires explicit documentation of:

- Whether ESG factors were considered and, if material, how they were incorporated

- Climate risk assessment applicability and methodology (for relevant asset classes)

- Data sources and their reliability assessment

- Restrictions on the valuation that might affect its use or reliability

- Any departures from IVS and their justification

This creates additional upfront work but substantially reduces disputes and regulatory challenges. In jurisdictions with active securities regulators, such as the UK's Financial Conduct Authority or the US Securities and Exchange Commission, enhanced documentation has proven crucial when valuations are challenged.

Uncertainty and Sensitivity Disclosure

IVS 103 now requires more robust disclosure of valuation uncertainty and sensitivity to key assumptions. This reflects lessons learned from the COVID-19 pandemic, when many valuations proved highly sensitive to assumptions that were treated as relatively certain.

Valuers must now provide:

- Qualitative assessment of overall valuation uncertainty (low, moderate, high)

- Quantitative sensitivity analysis for key value drivers

- Identification of assumptions with the highest impact on value

- Discussion of alternative scenarios when uncertainty is elevated

In practice, this means a typical valuation report now includes a sensitivity table showing value ranges under different scenarios. For a middle-market manufacturing company valued at $150 million, the report might show that value ranges from $125 million to $180 million depending on revenue growth assumptions (±3%) and EBITDA margin assumptions (±2%), with discount rate sensitivity adding another ±$15 million range.

06 Industry-Specific Implications

The IVS 2025 updates affect different industries and practice areas unevenly. Understanding these differential impacts is crucial for practitioners.

Private Equity and Venture Capital

Portfolio valuation practices face the most significant changes. The enhanced fair value guidance, combined with stricter documentation requirements, has increased the time and cost of quarterly valuations by an estimated 15-25% for most funds. However, this investment in rigor has also reduced disputes with limited partners and regulators.

For venture capital, the digital asset and intangible asset guidance provides much-needed structure for valuing early-stage technology companies where traditional metrics (revenue, EBITDA) are often absent or negative. The framework's emphasis on market participant assumptions helps address the persistent challenge of founder-optimism bias in management projections.

Financial Reporting and Purchase Price Allocations

Public companies performing purchase price allocations under IFRS 3 or ASC 805 benefit from IVS 2025's enhanced alignment with IFRS 13. The clarified fair value hierarchy and market participant guidance reduce ambiguity in identifying and valuing acquired intangible assets.

However, the ESG integration requirements create new challenges. For acquisitions in carbon-intensive industries, valuers must now explicitly consider transition risks when valuing long-lived assets, potentially affecting goodwill calculations and impairment testing.

Real Estate and Infrastructure

The climate risk assessment requirements have the most immediate impact on real estate and infrastructure valuations. Properties and assets with lives extending beyond 2040 now require scenario-based analysis of physical and transition climate risks.

This has led to valuation adjustments in specific submarkets. Coastal properties in high-risk flood zones have seen 5-12% valuation reductions when climate risk is properly incorporated. Conversely, energy-efficient buildings in low-risk locations have commanded premium multiples, with some institutional buyers paying 8-15% premiums for properties with strong sustainability credentials.

07 Implementation Challenges and Practical Solutions

Implementing IVS 2025 presents several practical challenges that valuation professionals must navigate.

Data Availability and Quality

The enhanced ESG and climate risk requirements demand data that is often unavailable or unreliable, particularly for private companies and emerging markets. Carbon emissions data, supply chain sustainability metrics, and climate scenario projections require specialized expertise and data sources.

Leading firms are addressing this through:

- Partnerships with ESG data providers (MSCI, Sustainalytics, Bloomberg ESG)

- Development of proprietary estimation models for missing data

- Clear documentation of data limitations and their impact on valuation reliability

Training and Competency Development

The breadth of new guidance—spanning digital assets, AI systems, climate risk, and ESG integration—exceeds the traditional training of many valuation professionals. Firms are investing heavily in continuing education, with the average valuation professional now completing 25-30 hours of IVS 2025-related training, compared to 10-15 hours for previous updates.

Technology and Tools

The complexity of IVS 2025 compliance has accelerated adoption of specialized valuation software. Platforms that automate documentation, perform sensitivity analysis, and integrate ESG data have seen adoption rates increase 40% in early 2025. Professional tools like iValuate have evolved to incorporate IVS 2025 requirements, helping practitioners efficiently navigate the enhanced standards while maintaining technical rigor.

08 Looking Forward: The Evolution of Valuation Standards

IVS 2025 represents a significant step forward in valuation practice, but it is not the final word. The IVSC has already signaled several areas for future development:

- Artificial Intelligence Valuation: As AI systems become more sophisticated and valuable, expect expanded guidance on valuing foundation models, AI-as-a-service platforms, and AI-generated content

- Nature-Related Financial Disclosures: Following the Taskforce on Nature-related Financial Disclosures (TNFD) framework, future IVS updates will likely address biodiversity and natural capital valuation

- Quantum Computing and Emerging Technologies: As quantum computing reaches commercial viability, valuation frameworks will need to address these transformative technologies

- Harmonization with Sustainability Standards: Greater alignment with the International Sustainability Standards Board (ISSB) standards as sustainability reporting becomes mandatory in more jurisdictions

For valuation professionals, staying ahead of these developments is not optional—it's essential to maintaining credibility and serving clients effectively. The profession is evolving from purely financial analysis to a more holistic assessment of value that incorporates environmental, technological, and social factors alongside traditional financial metrics.

09 Conclusion

The IVS 2025 updates represent the most significant evolution in international valuation standards in over a decade. The enhanced guidance on fair value measurement, ESG integration, climate risk assessment, and digital assets reflects the reality of modern business valuation—complex, multifaceted, and increasingly influenced by non-traditional factors.

For practitioners, these changes demand investment in new skills, data sources, and methodologies. The documentation burden has increased, and the technical complexity of many valuations has risen substantially. However, these enhancements also elevate the profession, providing clearer guidance for challenging situations and better alignment with the needs of stakeholders who rely on valuation conclusions.

The firms and professionals who embrace these changes—investing in training, technology, and process enhancement—will be best positioned to serve clients effectively in an increasingly complex valuation environment. Modern platforms like iValuate help professionals navigate these enhanced standards efficiently, ensuring compliance while maintaining the analytical rigor that defines excellent valuation work.

As we move through 2025 and beyond, the integration of ESG factors, climate considerations, and digital asset expertise into mainstream valuation practice will accelerate. The valuers who master these domains while maintaining technical excellence in traditional methodologies will define the next generation of valuation leadership.