Table of Contents11 sections

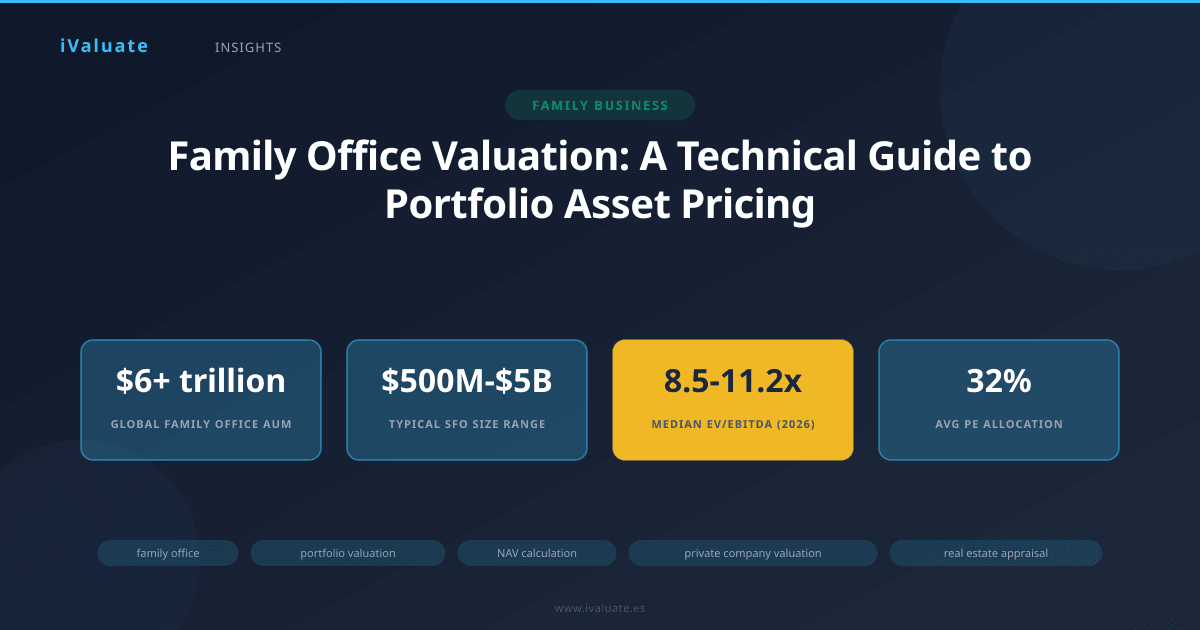

Family offices have emerged as one of the most significant pools of private capital in the global economy, with assets under management exceeding $6 trillion as of 2025. Unlike institutional investors bound by standardized reporting requirements, single-family offices (SFOs) and multi-family offices (MFOs) face unique valuation challenges across heterogeneous asset portfolios that often span operating businesses, commercial real estate, private equity stakes, and alternative investments.

The complexity of family office portfolio valuation has intensified in recent years due to rising interest rates, increased regulatory scrutiny, and the growing sophistication of ultra-high-net-worth (UHNW) families who demand institutional-grade reporting. This article provides a comprehensive technical framework for valuing the three primary asset classes within family office portfolios: operating companies, real estate holdings, and investment portfolios.

01 The Family Office Landscape and Valuation Imperatives

Family offices operate under fundamentally different constraints than institutional asset managers. A typical SFO manages between $500 million and $5 billion for a single family, while MFOs serve multiple families with aggregate assets often exceeding $10 billion. According to the 2025 Global Family Office Report, 68% of family offices hold direct stakes in operating companies, 82% maintain significant real estate portfolios, and virtually all manage diversified investment portfolios including public securities, private equity, and alternatives.

The valuation imperative stems from multiple sources. First, accurate net asset value (NAV) calculations are essential for wealth planning, estate tax compliance, and intergenerational transfers. Second, families increasingly require performance attribution across asset classes to make informed allocation decisions. Third, when family offices contemplate liquidity events—selling operating companies, refinancing real estate, or rebalancing portfolios—precise valuations become critical negotiating tools.

Family offices managing over $1 billion typically conduct comprehensive portfolio valuations quarterly, with annual independent appraisals for material holdings. This frequency has increased 40% since 2020 as families demand greater transparency.

02 Valuing Operating Companies Within Family Office Portfolios

Operating companies represent the most complex valuation challenge for family offices, particularly when these businesses were founder-built and remain closely held. Unlike publicly traded companies with observable market prices, private operating companies require application of multiple valuation methodologies to triangulate fair market value.

Income Approach: Discounted Cash Flow Analysis

The discounted cash flow (DCF) method remains the gold standard for valuing mature, cash-generating operating companies. For a family office holding a manufacturing business generating $50 million in annual EBITDA, the DCF process involves projecting unlevered free cash flows over a 5-10 year period and discounting them to present value using a weighted average cost of capital (WACC).

In the current environment (Q1 2026), WACC calculations have become particularly sensitive to interest rate assumptions. With the 10-year Treasury yield hovering around 4.2%, risk-free rates have stabilized after the volatility of 2022-2024. For a typical middle-market operating company within a family office portfolio, we observe WACC ranges of 10-14%, depending on industry risk, company size, and capital structure.

The terminal value calculation deserves special attention in family office contexts. Unlike institutional investors who may assume exit within 5-7 years, family offices often hold operating companies indefinitely. This requires careful consideration of perpetuity growth rates—typically 2.5-3.5% in developed markets—and sensitivity analysis around terminal value assumptions, which commonly represent 60-75% of total enterprise value.

Market Approach: Comparable Company and Transaction Analysis

The market approach provides critical validation for DCF valuations. Family offices typically employ two market-based methodologies: comparable public company analysis and precedent transaction analysis.

For comparable company analysis, the challenge lies in identifying truly comparable businesses. A family office holding a regional consumer products company must adjust public company multiples for size (typically a 20-30% discount for companies under $100 million in revenue), liquidity (an additional 15-25% discount for private companies), and geographic concentration. As of early 2026, median EV/EBITDA multiples for middle-market consumer companies range from 8.5x to 11.2x, down from the 12-15x peaks of 2021 but recovering from the 7-9x trough of late 2023.

Precedent transaction analysis examines actual M&A transactions in the relevant industry. Family offices should focus on transactions within the past 24-36 months, adjusting for deal-specific factors such as strategic buyer premiums (typically 20-35% above financial buyer valuations) and control premiums (generally 25-40% for majority stakes).

Asset Approach: Net Asset Value for Holding Companies

When a family office's operating company functions primarily as a holding company for subsidiaries or real estate, the asset approach becomes relevant. This method involves valuing each underlying asset separately and summing to arrive at total enterprise value, then subtracting liabilities to determine equity value.

Consider a family office holding company with three operating subsidiaries valued at $80 million, $45 million, and $30 million respectively, plus commercial real estate worth $120 million and net debt of $75 million. The equity value would be $200 million ($275 million in assets minus $75 million in debt). This approach is particularly common among European family offices, where holding company structures dominate for tax efficiency.

03 Real Estate Portfolio Valuation Methodologies

Real estate typically represents 25-40% of family office portfolios, encompassing everything from trophy office buildings and industrial warehouses to residential developments and agricultural land. The valuation approach varies significantly by property type, but three core methodologies dominate.

Income Capitalization Approach

For stabilized, income-producing properties, the direct capitalization method provides the most straightforward valuation. Net operating income (NOI) is divided by a capitalization rate to determine property value. The critical challenge lies in selecting appropriate cap rates, which have compressed significantly over the past decade but began normalizing in 2024-2025.

As of Q1 2026, cap rates for institutional-quality office properties in gateway cities range from 5.5-7.5%, while industrial properties command 4.5-6.0% cap rates due to continued e-commerce demand. Retail properties show the widest dispersion, from 6.0% for grocery-anchored centers to 9.0%+ for struggling malls. Family offices must adjust these market cap rates for property-specific factors including tenant credit quality, lease duration, and deferred maintenance.

For a family office holding a 250,000 square foot industrial property generating $4.5 million in NOI, a 5.2% cap rate would yield a valuation of approximately $86.5 million. However, if the property has significant lease rollover in the next 24 months or requires capital improvements, the cap rate might be adjusted to 5.8%, reducing the valuation to $77.6 million.

Discounted Cash Flow for Development and Value-Add Properties

When family offices hold development projects or value-add properties requiring significant capital investment, DCF analysis becomes essential. This involves projecting property-level cash flows over the anticipated hold period (typically 5-10 years for value-add, 2-5 years for development), including rental income growth, operating expense inflation, capital expenditures, and terminal sale proceeds.

Discount rates for real estate DCF analysis currently range from 8-12% depending on risk profile. Core properties in primary markets might warrant 8-9% discount rates, while opportunistic developments could require 11-13%. The terminal cap rate assumption—typically 50-100 basis points higher than the entry cap rate—significantly impacts valuation outcomes.

Sales Comparison Approach

For unique properties or thin markets, the sales comparison approach examines recent transactions of comparable properties. Family offices holding residential real estate, agricultural land, or specialty properties often rely heavily on this method. The key is making appropriate adjustments for differences in location, size, condition, and timing.

A family office valuing a 500-acre agricultural property might examine recent sales of similar farmland in the region, which in prime Midwest locations have traded at $12,000-$15,000 per acre in 2025-2026, up from $8,000-$11,000 in 2020. Adjustments would be made for soil quality, water rights, existing improvements, and proximity to markets.

04 Investment Portfolio Valuation: From Public Securities to Alternatives

While publicly traded securities have readily observable market prices, family office investment portfolios present valuation challenges in three areas: private equity stakes, hedge fund investments, and alternative assets.

Private Equity and Venture Capital Holdings

Family offices increasingly allocate to private equity, with the average allocation reaching 32% in 2025 according to UBS Family Office Survey data. Valuing these positions requires understanding the underlying portfolio companies and applying appropriate valuation methodologies.

For direct private equity investments, family offices should employ the same operating company valuation techniques discussed earlier. For fund investments (LP stakes in PE funds), valuation depends on the fund manager's reporting. Established funds typically provide quarterly NAV statements based on portfolio company valuations, but family offices should scrutinize the methodologies and assumptions.

A critical consideration is the J-curve effect in venture capital and growth equity investments. Early-stage companies may be valued at cost or recent financing rounds, but these valuations can be stale. A family office holding a $10 million stake in a Series B company last valued at $200 million pre-money might need to consider whether that valuation remains supportable 18 months later, particularly if the company has missed growth targets or market conditions have deteriorated.

Hedge Funds and Alternative Investment Vehicles

Hedge fund investments typically report monthly or quarterly NAV figures, but family offices should understand the underlying valuation policies, particularly for funds holding illiquid securities. Long-short equity funds with liquid positions present minimal valuation concerns, but credit funds, distressed debt strategies, and structured products require deeper scrutiny.

For alternative investments including private credit, infrastructure, and natural resources, family offices should request detailed valuation reports and understand whether valuations are based on discounted cash flow models, market comparables, or third-party appraisals. Infrastructure investments, for example, are typically valued using DCF with discount rates of 7-10% depending on regulatory environment, contract structure, and operational risk.

Cryptocurrency and Digital Assets

An emerging challenge for family offices is valuing cryptocurrency and digital asset holdings. While Bitcoin and Ethereum have observable spot prices on major exchanges, family offices must address several technical issues: which exchange price to use (prices can vary 1-3% across venues), how to value staked assets (which may be locked for periods), and how to account for tokens in DeFi protocols where liquidity is limited.

For family offices holding material cryptocurrency positions—some now allocate 3-8% to digital assets—best practice involves using volume-weighted average prices from multiple reputable exchanges and applying liquidity discounts for large positions that could move markets if liquidated. A family office holding $50 million in Bitcoin should consider that liquidating such a position could incur 2-4% in market impact costs, which should be reflected in the NAV calculation.

05 Consolidated NAV Calculation and Reporting

The ultimate objective of family office valuation is producing an accurate, defensible net asset value calculation that aggregates all portfolio holdings. This requires a systematic approach to consolidation, elimination of intercompany holdings, and appropriate treatment of liabilities.

A comprehensive family office NAV statement typically includes:

- Operating Companies: Valued using DCF, market multiples, or asset-based approaches, with clear documentation of methodologies and key assumptions

- Real Estate Holdings: Valued using income capitalization, DCF, or sales comparison, with independent appraisals for properties exceeding $25-50 million in value

- Public Securities: Marked to market using closing prices from primary exchanges

- Private Equity and Funds: Based on most recent fund NAV statements, adjusted for capital calls and distributions

- Alternative Investments: Valued using manager-provided NAVs or independent appraisals

- Cash and Cash Equivalents: At face value

- Liabilities: Including debt at face value (or fair value if significantly different), deferred taxes, and contingent liabilities

The consolidated NAV calculation must also address intercompany eliminations. If the family office holding company has lent $20 million to an operating subsidiary, this loan appears as an asset at the holding company level and a liability at the subsidiary level. Proper consolidation requires eliminating both to avoid double-counting.

06 Valuation Frequency and Independent Verification

Leading family offices have adopted institutional-grade valuation practices, including quarterly internal valuations and annual independent appraisals for material assets. For operating companies generating over $10 million in EBITDA, annual third-party valuations have become standard practice, with many families requiring independent valuation every 2-3 years even for smaller holdings.

Real estate portfolios typically undergo annual appraisals for properties valued above $25 million, with desktop valuations or automated valuation models (AVMs) used for smaller properties. The cost of comprehensive independent valuation—typically $15,000-$50,000 per operating company and $5,000-$25,000 per real estate property—is justified by the improved decision-making and risk management these valuations enable.

Family offices with robust valuation processes report 23% higher risk-adjusted returns over 10-year periods compared to those with ad-hoc valuation practices, according to 2025 research from the Family Office Association.

07 Case Studies: Real-World Applications

Case Study 1: Manufacturing Company Valuation Complexity

A European single-family office held a 75% stake in a specialty chemicals manufacturer generating €40 million in revenue and €8 million in EBITDA. The company had grown organically at 6% annually but faced margin pressure from rising energy costs. The family office engaged in a comprehensive valuation to consider potential sale or recapitalization.

The DCF analysis projected cash flows over 10 years, assuming 4% revenue growth and gradual margin recovery as energy efficiency investments took effect. Using a WACC of 11.5%, the DCF yielded an enterprise value of €72 million. Comparable company analysis suggested EV/EBITDA multiples of 8.5-10.5x for similar businesses, implying a range of €68-84 million. Recent transactions in the sector showed multiples of 9.2x, supporting a €73.6 million valuation.

The family office adopted a €72 million enterprise value, implying €54 million for their 75% stake after adjusting for net debt. This valuation informed their decision to pursue a minority recapitalization, selling 25% to a financial sponsor at a 15% premium to the standalone valuation, reflecting the control premium and growth capital the sponsor would provide.

Case Study 2: Mixed-Use Real Estate Portfolio

A North American multi-family office managed a $380 million real estate portfolio for three families, comprising 12 properties across office, retail, and industrial sectors. The office implemented quarterly valuations using a combination of income capitalization for stabilized properties and DCF for value-add assets.

One property—a 180,000 square foot office building in a secondary market—presented particular challenges. Occupancy had declined from 92% to 78% as two major tenants downsized. The property generated $3.2 million in NOI, but required $4.5 million in tenant improvements and leasing commissions to stabilize occupancy. A simple cap rate approach using the market rate of 7.0% would yield a $45.7 million valuation, but this ignored the near-term capital requirements and vacancy risk.

The family office instead employed a DCF analysis, projecting gradual lease-up over 30 months, incorporating the capital expenditures, and using an 8.5% discount rate to reflect the elevated risk. This approach yielded a $38.2 million valuation—16% below the simple cap rate method—which better reflected the property's true economic value and informed the decision to either invest the required capital or divest the asset.

Case Study 3: Private Equity Portfolio Valuation Dispute

An Asian family office had invested $25 million across five private equity funds between 2019 and 2022. By Q4 2025, the funds reported an aggregate NAV of $31.8 million, representing a 27% gain. However, the family office's advisors questioned whether these valuations reflected the changed market environment, particularly for technology investments that had been marked up significantly during 2020-2021.

A detailed review revealed that one fund, representing $8 million of the original commitment, had not updated valuations for three portfolio companies in over 12 months despite significant deterioration in public market comparables. The family office engaged an independent valuation firm to assess these holdings, which concluded that appropriate markdowns of 25-35% were warranted, reducing the fund's NAV by approximately $2.1 million.

This experience led the family office to implement enhanced due diligence procedures for private equity investments, including quarterly calls with fund managers to discuss valuation methodologies and semi-annual independent reviews of the largest positions.

08 Technology and Tools for Family Office Valuation

The complexity of family office portfolio valuation has driven adoption of specialized technology platforms. While many family offices historically relied on spreadsheets and manual processes, leading families now employ integrated portfolio management systems that consolidate data from multiple sources, apply consistent valuation methodologies, and generate comprehensive reporting.

These platforms typically integrate market data feeds for public securities, incorporate private company valuation models with sensitivity analysis, and maintain detailed records of valuation assumptions and methodologies. For real estate portfolios, integration with property management systems enables automated NOI calculations and cap rate analysis.

Advanced family offices are also leveraging artificial intelligence and machine learning to enhance valuation processes. Natural language processing can extract key terms from lease agreements and loan documents, while machine learning models can identify comparable companies and transactions more efficiently than manual research. However, these technologies complement rather than replace professional judgment—the selection of appropriate methodologies, key assumptions, and risk adjustments remains fundamentally a human exercise requiring deep expertise.

09 Regulatory and Tax Considerations

Family office valuations carry significant regulatory and tax implications that vary by jurisdiction. In the United States, accurate valuations are essential for estate and gift tax compliance, with the IRS closely scrutinizing valuations that appear aggressive. The Tax Cuts and Jobs Act of 2017 increased the estate tax exemption to $13.61 million per individual (as of 2024, inflation-adjusted), but this is scheduled to sunset in 2026, creating urgency for families to complete intergenerational transfers at defensible valuations.

For international family offices, transfer pricing regulations require arm's-length valuations for intercompany transactions. A family office with operating companies in multiple jurisdictions must ensure that management fees, royalties, and other intercompany charges are supported by robust valuation analysis to withstand tax authority scrutiny.

The Foreign Account Tax Compliance Act (FATCA) and Common Reporting Standard (CRS) have increased reporting requirements for family offices with international holdings, making accurate valuations essential for compliance. Penalties for underreporting can reach 40% of the tax underpayment, making the cost of professional valuation services a prudent investment.

10 Best Practices and Governance Framework

Leading family offices have established formal valuation governance frameworks that include:

- Valuation Policy: A written document specifying valuation methodologies for each asset class, frequency of valuations, and thresholds for independent appraisals

- Valuation Committee: A dedicated committee (often including family members, external advisors, and independent experts) that reviews and approves significant valuations

- Documentation Standards: Comprehensive documentation of valuation assumptions, methodologies, and supporting analysis for each material holding

- Independent Review: Periodic engagement of independent valuation firms to review internal valuations and provide objective assessments

- Sensitivity Analysis: Regular stress-testing of valuations under different scenarios (recession, interest rate changes, industry disruption)

These governance practices not only improve valuation accuracy but also provide defensibility in the event of tax audits, family disputes, or litigation. The cost of implementing robust valuation governance—typically $100,000-$500,000 annually for a family office managing $1-5 billion—is modest relative to the potential costs of valuation disputes or suboptimal decision-making based on inaccurate valuations.

11 Looking Forward: The Evolution of Family Office Valuation

As family offices continue to grow in size and sophistication, valuation practices will evolve in several directions. First, the integration of environmental, social, and governance (ESG) factors into valuation models is accelerating. Operating companies with strong ESG profiles command premium valuations—recent research suggests a 10-15% valuation premium for companies in the top ESG quartile—and family offices are increasingly incorporating ESG assessments into their valuation frameworks.

Second, the rise of digital assets and tokenization will create new valuation challenges and opportunities. Some family offices are exploring tokenization of real estate and private equity holdings to enhance liquidity, but this requires new approaches to valuation that account for token-specific factors including smart contract terms, blockchain infrastructure, and regulatory treatment.

Third, artificial intelligence and alternative data sources will enhance valuation precision. Satellite imagery can assess retail traffic patterns and industrial facility utilization, while web scraping can provide real-time data on consumer sentiment and competitive positioning. These data sources, combined with traditional financial analysis, will enable more accurate and timely valuations.

The increasing complexity of family office portfolios and the rising stakes of accurate valuation have made professional-grade tools essential. Platforms like iValuate enable family offices to perform sophisticated valuation analysis efficiently, applying institutional-quality methodologies to operating companies, real estate, and investment portfolios. As families demand greater transparency and more frequent reporting, the ability to generate defensible valuations quickly and consistently has become a competitive advantage in family office management.

For family offices navigating the challenges of portfolio valuation in 2026 and beyond, the path forward requires combining rigorous technical methodologies with practical judgment, supported by appropriate technology and governance frameworks. The families that invest in building these capabilities will be better positioned to preserve and grow wealth across generations, make informed allocation decisions, and navigate the increasingly complex landscape of global investing.